A 409A valuation for startups gets harder when revenue depends on usage meters and outcome clauses. Your board still needs a fair market value for common stock on the option grant date.

AI SaaS deals often mix subscriptions, usage charges, and performance fees. That mix changes revenue predictability and gross margin behavior in the same quarter.

This article explains the exact friction points. It also shows what data makes the valuation smoother and more defensible.

The job of a 409A valuation

A 409A valuation estimates the fair market value of a private company’s common stock. A company uses that value to set stock option exercise prices at or above fair market value on the grant date.

The analysis ties to facts on a specific valuation date. The report explains the methods and inputs used on that date.

A prior valuation does not stay reasonable when new material information affects value and a prior valuation also does not stay reasonable when the valuation date sits more than 12 months before the later grant.

Why “safe harbor” matters to founders and employees

Certain valuation approaches create a presumption that the value is reasonable while independent appraisals often support that presumption in practice.

The presumption can be challenged by the tax authority. The challenge focuses on whether the method or its use is grossly unreasonable.

A strong record helps the company and a clean record also protects option recipients from discount claims.

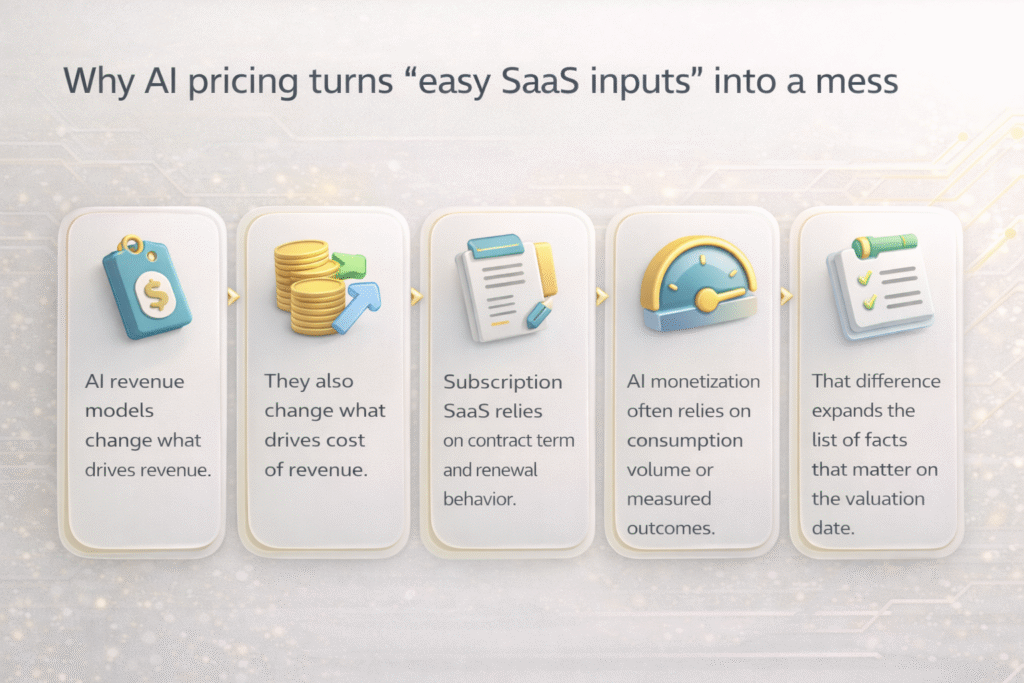

Why a 409A valuation for startups looks different once AI revenue enters the picture

Subscription SaaS revenue ties to a contract term and a renewal cycle. AI revenue is often tied to customer activity or measured results.

These activities change fast and the results depend on definitions, acceptance steps, and remedy clauses.

Valuation teams still need a clean revenue view for the forecast. They also need a clean cost view for gross margin and cash flow expectations.

This is where SaaS plus AI hybrids create extra work, because the business does not map neatly to simple multiples.

The moment clean SaaS multiples start to wobble

Revenue multiples work best when you compare like with like. That comparison depends on similar revenue quality and similar revenue definitions across the peer set.

Classic SaaS uses recurring contract commitments as the anchor. AI driven pricing often uses consumption volume as the anchor, so the same label can behave differently month to month.

Outcome based deals add another layer, because the contract can change what gets billed based on measured performance.

Once the revenue story changes shape, the multiple loses clarity. Then the valuation relies more on drivers, scenarios, and contract evidence.

Usage-based revenue changes what “recurring” means

Usage-based pricing ties revenue to consumption in a billing period . The consumption changes with workflow volume and customer policy.

Teams often translate usage revenue into an annualized run rate and the run rate depends on the chosen time window. A 30-day window reacts to spikes while a 90-day window smooths spikes and hides sudden shifts.

A defensible report needs one definition for run rate and that definition needs consistent use across board decks and finance reports.

Common usage drivers that show up in AI SaaS billing

- API calls per account

- Tokens consumed per workflow

- Minutes processed per agent

- Tickets handled per month

- Documents analyzed per day

- Messages generated per user

Each driver explains the revenue movement and also the cost movement when modeling access prices by unit.

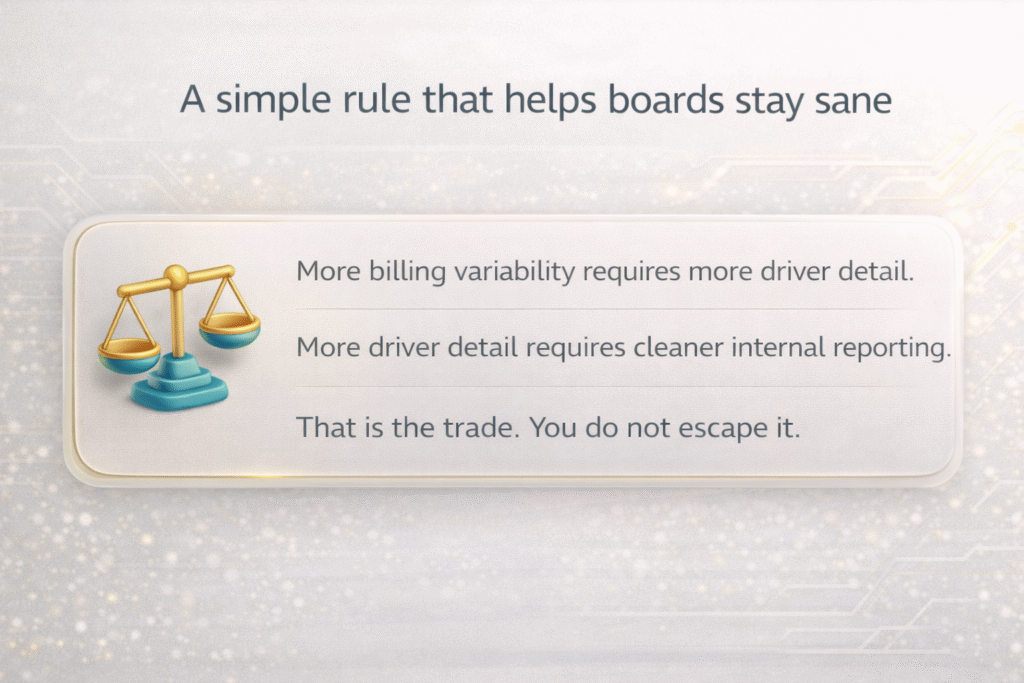

This is why a 409A valuation for startups needs usage cohorts. A single revenue line does not explain the business.

Outcome-based pricing adds measurement rules and real downside terms

Outcome pricing ties fees to a measured result. The contract defines the result and the measurement method.

In practice, contracts can require acceptance steps. Contracts can also include penalties, refunds, or credits tied to performance.

Revenue accounting treats many of these structures as variable consideration. Under that framework, the constraint concept limits recognized revenue when reversal risk stays meaningful.

A valuation forecast should follow the same discipline. For that reason, the forecast should separate committed minimums from variable upside. This separation improves clarity for the board. It also reduces rework during audit review.

Hybrid contracts carry two revenue personalities inside one logo

Many AI SaaS contracts include a subscription minimum plus overages. The minimum behaves like committed recurring revenue.

At the same time, the overage behaves like consumption revenue. The overage can jump without new logos. This structure complicates retention reporting. Expansion becomes more usage, not more seats, in many accounts.

Hybrid contracts also raise concentration risk. One large customer can drive most usage and most costs in a period.

A 409A valuation for startups needs a view of minimum coverage. It also needs overage sensitivity by top accounts.

Variable AI costs move with volume, and margin shifts follow

Many AI businesses pay model or compute providers per token or per request. That structure makes the cost of revenue rise with usage volume. As usage climbs, revenue can rise in the same month. Costs can rise in the same month too.

Gross margin percent can shift quickly. Gross margin affects cash flow expectations and risk assessment in valuation work.

Margin changes also affect peer comparisons. A high growth line looks different when the margin compresses. This pattern shows up most in SaaS plus AI hybrids. It also shows up during rapid product releases.

Deal features that trigger extra valuation questions

- Subscription minimum plus usage overages

The minimum creates a committed floor. The overage depends on consumption behavior. - Prepaid credits with drawdown patterns

Credits shift timing through deferred revenue. Drawdown shapes seasonality. - Customer caps and throttles

Caps limit growth without churn. Throttles change revenue and cost in the same period. - Service credits tied to uptime or accuracy

Credits reduce billed amounts under stated conditions. Credits create a downside case for the forecast. - Bonuses and penalty clauses tied to results

These clauses change the total consideration. These clauses require a written metric definition. - Refund rights tied to acceptance or performance

Refund rights increase downside risk. Refund rights also affect forecast confidence. - Tiered model pricing by quality level

Tier mix changes average price per unit. Tier mix changes the margin by cohort. - Non-standard enterprise terms

Custom terms reduce comparability across customers. Custom terms increase one-off risks. - High usage concentration in a few accounts

Concentration increases sensitivity to customer behavior. Concentration also increases the volatility in the cost of revenue.

Taken together, each item changes the forecast which also changes the story that a valuation team must document.

One table that makes alignment easy across finance, legal, and the valuation firm:

| Revenue model type | Main billing driver | Valuation input that gets harder | Evidence that helps the analysis |

| Subscription SaaS | Seats and contract term | Renewal stability and retention | Cohort retention, churn definition, and bookings history |

| Usage-based AI SaaS | Consumption volume | Run rate definition and usage drivers | Usage cohorts, seasonality, top account sensitivity |

| Outcome-based AI SaaS | Measured results | Variable fees and downside terms | Metric definition, acceptance rules, credit, and refund terms |

| Hybrid minimum plus usage | Minimum plus overage | Mix stability and margin stability | Minimum coverage, overage history, and margin by tier |

This table helps a 409A valuation for startups stay on schedule. It also reduces back and forth during draft review.

What to prepare before your 409A process starts

- Cap table and equity plan documents

The valuation needs the capital structure on the valuation date. The valuation also needs award plan terms. - All financing documents, notes, and SAFEs

Terms affect allocation between preferred and common. Allocation drives common stock value. - A written definition of recurring revenue

The definition must match internal reporting. The definition must match board reporting. - A written definition of usage run rate

The definition must include the time window. The definition must specify what counts as usage. - Revenue by cohort and by contract type

Cohorts show retention and expansion. Contract types explain volatility sources. - Usage data by cohort and top accounts

Usage supports volume forecasting. Top account data supports concentration analysis. - Gross margin by product line and pricing tier

Margin by tier shows unit economics differences. Unit economics support forecast assumptions. - Representative contracts and the biggest exceptions

Contracts define credits, caps, and penalties. Exceptions explain outlier behavior. - Driver-based forecast with stated assumptions

Drivers tie revenue to activity or results. Assumptions create a record for reasonableness review. - A short list of value-changing events since the last report

Events include financings and major contracts. Events also include product changes that alter unit economics.

This package makes a 409A valuation for startups cleaner. It also reduces revision cycles near a grant date.

Why preferred pricing and common value can sit far apart in AI hybrids

Venture financings often price preferred stock which often carries rights that common stock does not carry. Because of those rights, liquidation preferences change the payout order in an exit. Protective provisions can change economic outcomes as well.

These rights affect how total equity value is allocated across share classes. A wider forecast spread can increase the impact of scenario outcomes on allocation. This result does not signal an error. It reflects differences in rights and risk exposure.

FAQ

Does a pricing model change force a new 409A valuation for startups

A valuation becomes unreasonable when it fails to reflect new material information. A pricing change can become material when it changes revenue expectations and margin behavior on the valuation date.

Does usage revenue work in a 409A valuation for startups

A 409A valuation for startups can use usage revenue as an input. The analysis needs a stable run rate definition and evidence that supports the usage drivers used in the forecast.

Do outcome-based contracts change how forecasts work

Outcome contracts often include variable consideration features. Forecasts should separate committed minimums from variable upside tied to measurement, acceptance, and downside terms.

How long does a 409A valuation stay usable?

A valuation date older than 12 months does not support a later option grant under the timing rule. New material information can also require a refresh every 12 months.

Contact Bookman Capital

A 409A valuation for startups needs clear definitions when revenue mixes subscriptions, usage, and outcomes. Bookman Capital helps founders and finance teams document revenue drivers, align forecast inputs, and support defensible common stock fair market value. Contact Bookman Capital today.

Sources:

26 CFR § 1.409A-1 (Treasury Regulations on 409A valuations)

26 U.S.C. § 409A (U.S. Code)

Deloitte ASC 606 Roadmap: Variable Consideration (Step 3)