Here’s something most SaaS founders discover too late: there’s a simple formula that can mean the difference between selling your company for $20 million versus $60 million. What is the Rule of 40, and why does it matter so much to your company’s valuation?

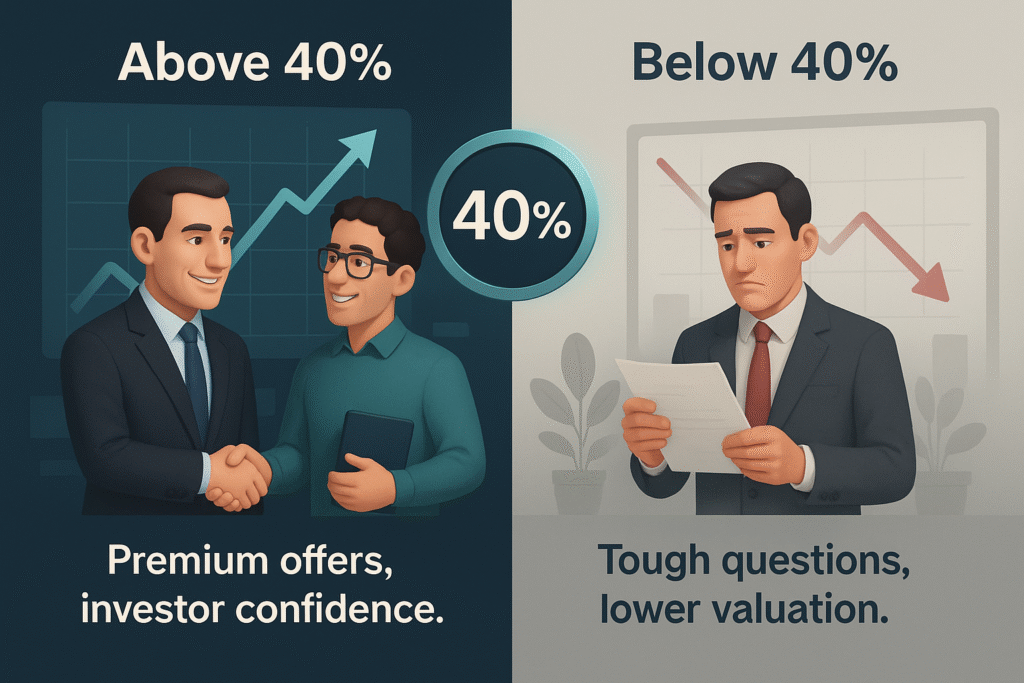

Think of it like a credit score for your company. Just as your personal credit score determines whether you qualify for a mortgage, your Rule of 40 score determines whether investors will even take a meeting with you. Score above 40. Suddenly, you’re fielding multiple offers, often with premium valuations attached. Score below that mark and you might spend months explaining why your business deserves a second look.

Why is the Rule of 40 significant? The answer is straightforward: it demonstrates to investors that a company has achieved rapid growth without uncontrolled cash burn. It’s the business equivalent of proving you can sprint without collapsing at the finish line.

So what exactly is this number?

Where the Rule of 40 Actually Came From

Brad Feld from Techstars first articulated this pattern in his 2015 blog post ‘Rule of 40% For a Healthy SaaS Company,’ where he noticed a pattern in the best-performing SaaS companies he studied. The best-performing SaaS companies he studied all shared something unusual. Their revenue growth rate plus profit margin consistently added up to 40% or more.

That observation became the Rule of 40. Add your annual revenue growth percentage to your EBITDA margin percentage. If you hit 40 or above, you’re in good shape. Fall short, and investors start asking tough questions about your business model.

The formula spread fast. Today, these investors filter thousands of opportunities through this single metric before looking at anything else.

The 40% threshold remains somewhat debated among analysts. But most agree it separates strong SaaS companies from weak ones. Hitting this number proves you can balance growth and profitability, which is genuinely difficult to achieve. It signals that management understands their unit economics instead of just spending money hoping for results.

Why This Uses EBITDA Instead of Regular Profit

EBITDA levels the playing field by focusing purely on operating performance before financing decisions come into play. Every SaaS company structures itself differently with debt, leases, and equipment purchases that affect net income and make direct comparisons meaningless. EBITDA captures what’s really happening with your operations instead of getting tangled up in accounting rules that don’t reflect reality for subscription businesses.

The Valuation Gap That Should Keep You Up at Night

Here’s where this gets really interesting. Companies that beat the Rule of 40 don’t just get slightly better valuations. They get offers that are two to three times higher than companies that don’t. We’re not talking theory here. Software Equity Group tracks this across thousands of actual transactions.

Right now in 2025, according to SaaS Capital’s Index data, the typical private SaaS company sells for about 4.1 times its annual recurring revenue. But if you’re hitting that Rule of 40 benchmark? You’re looking at seven to twelve times revenue. On a company doing $5 million in ARR, that’s literally the difference between a $20 million exit and a $60 million exit.

Want to know something sobering? The median Rule of 40 score right now is estimated to sit at 12%. Most companies are averaging around 10% growth and 6% profit margin. These numbers can fluctuate based on market cycles, but the pattern holds: the vast majority of SaaS founders are leaving millions of dollars on the table without even realizing it.

Investors aren’t paying those premiums out of generosity. Higher scores mean lower risk for them. It signals sustainable growth instead of the kind that collapses the moment you stop spending money. Importantly, it shows a clear path to profitability instead of a business model held together with duct tape and hope.

5 Calculation Mistakes That Destroy Your Score’s Credibility

Getting your Rule of 40 score right matters more than you think. Here are the mistakes that sabotage even strong businesses:

- Comparing Yourself to Companies at Different Stages – Benchmark against companies at similar revenue stages with similar business models, because your early-stage startup with $2 million in ARR shouldn’t compare itself to a mature company doing $50 million in ARR.

- Mixing Recurring and One-Time Revenue – Only count genuinely recurring subscription revenue in your growth calculation, not implementation fees or one-time professional services that artificially inflate your numbers.

- Cherry Picking Your Best Quarter – Use trailing 12-month data instead of showcasing a single stellar quarter, because investors want to see sustainable growth patterns that smooth out seasonal variations.

- Ignoring Customer Churn in Growth Calculations – Always calculate net new ARR by subtracting churned revenue from new bookings, since failing to account for churn gives you an inflated growth rate that collapses under scrutiny.

- Using Gross Profit Instead of EBITDA – EBITDA accounts for all operating expenses including sales, marketing, and product development, while gross profit only subtracts direct delivery costs and can inflate your profitability margin by 30 to 50 percentage points.

| Scenario | Growth Rate | EBITDA Margin | Rule of 40 Score | What Investors Think |

| Hypergrowth Startup | 50% | -10% | 40% | Acceptable if the burn rate makes sense |

| Balanced Performer | 25% | 15% | 40% | Extremely attractive and sustainable |

| Mature Cash Generator | 10% | 30% | 40% | Decent but limited upside potential |

| Reckless Growth | 80% | -40% | 40% | Red flags everywhere despite hitting 40 |

Note: These scenarios demonstrate that hitting 40% alone isn’t sufficient. The composition and sustainability of the score matter significantly to investors.

When You Should Actually Care About This Number

The Rule of 40 matters most when your company sits somewhere between $15 million and $50 million in annual recurring revenue. Before that range, other things matter more. After that range, investors simply expect you to be above 40% consistently.

If you’re still in the early stages, obsessing over this metric is honestly a waste of time. Your numbers will swing wildly while you’re figuring out product market fit. One month you’ll sign five customers, the next month you’ll sign none. Small changes in revenue create percentage swings that look terrifying on paper but don’t really mean anything yet.

Brad Feld himself recommends you start taking this seriously once you cross $12 million in ARR. By that point, you’ve probably built out your core teams: sales, marketing, customer success, and product development. At that stage, operational efficiency becomes something you can actually measure meaningfully.

Here’s a trap to watch out for, though. High scores can be deceiving. Imagine a company growing at 80% but burning through 40% negative margins. Technically, they hit 40%, right? But that burn rate is completely unsustainable. Investors aren’t fooled. They can spot the difference between a healthy balance and someone gaming the math.

What Good Looks Like at Each Stage

When you’re below $5 million in ARR, forget about the Rule of 40 entirely. Focus everything on product market fit. Growing at 40% or more makes perfect sense even if you’re losing money. Investors expect losses at this stage.

Companies in the $5 million to $25 million range should start paying attention. You don’t need to be above 40% yet, but you should see the trend moving in the right direction. Investors still prioritize growth over profitability here. However, they want to see efficiency improve over time.

Once you cross $25 million in ARR, this metric becomes central to every investor conversation. Consistently scoring below 40% at this stage signals something is fundamentally broken in your business model.

And if you’re approaching an exit above $50 million in ARR, you really want to be hitting 45% or higher. That’s what gets you premium offers from strategic buyers and private equity firms.

Other Numbers That Actually Matter More Sometimes

Though significant, the Rule of 40 isn’t always the most important metric investors examine. Here are the other numbers one should pay attention to:

- Annual Churn Rate – Keep annual churn below 6% and you’ve demonstrated real product stickiness.

- Net Revenue Retention (NRR) – Companies with NRR above 120% command 11.7 times median valuations compared to just 5.6 times for everyone else.

- Gross Margins – Get above 80% gross margins and you’re looking at 7.6 times revenue multiples versus 5.5 times for lower margins.

- Customer Acquisition Cost (CAC) Payback Period – Getting to payback in under 12 months proves your sales and marketing machine works.

6 Strategies to Engineer Your Score Higher in the Next 90 Days

Improving your Rule of 40 isn’t about accounting tricks or creative math. It’s about making strategic operational changes that genuinely improve your business fundamentals.

Add Usage-Based Pricing Tiers – Usage-based pricing that charges for API calls, transactions, or storage automatically grows revenue as customers succeed, creating expansion revenue that improves your growth rate without additional sales effort, customer success, creating a virtuous cycle.

Switch to Annual Upfront Billing – When customers pay annually upfront instead of monthly, your cash flow improves immediately and you recognize the full year’s EBITDA impact right away. Companies that make this switch typically see 15 to 25% improvement in cash flow metrics within the first quarter.

Focus Customer Success on Expansion Revenue – Shift 30% of your customer success team’s focus toward identifying upsell and cross-sell opportunities, since expansion revenue from existing customers costs five times less than new customer acquisition.

Audit and Eliminate SaaS Tool Sprawl – Conduct a 30-day audit of every software subscription your company pays for and you’ll likely find redundant tools that nobody uses. Cutting these typically saves 5 to 15% on operating expenses, which flows directly to EBITDA margin.

Renegotiate Cloud Hosting Contracts – Reserved instances from AWS, Azure, or Google Cloud save 30 to 50% compared to on-demand pricing, and right-sizing your instances cuts another 10 to 20%. A thorough cloud cost optimization project delivers 10 to 20% infrastructure savings within 60 days.

Implement Product-Led Growth to Lower CAC – Build self-service onboarding flows where users can sign up and find value without talking to sales, which can drop customer acquisition costs by 30 to 50% while your growth rate actually accelerates.

What Actually Happens When Investors Look at Your Numbers

The Rule of 40 functions as an initial gate. Pass it, and investors move forward with deeper analysis. Fail it, and you’ll need compelling explanations for why they should keep talking to you.

Different types of investors use this metric differently. Private equity firms typically demand consistent performance above 40% before they’ll even consider an acquisition. Venture capitalists are more flexible with early-stage companies, as long as they see clear improvement trajectories.

But here’s the reality: the complete evaluation involves 20 or more factors beyond just the Rule of 40. A strong score opens doors, but it definitely doesn’t guarantee premium offers. Valuations are influenced by more than just benchmark metrics, and smart investors know that context matters enormously.

Red flags can make even impressive scores concerning. That is why nvestors conduct a quality of earnings analysis specifically to verify that your performance is sustainable.

The Reality Check That Comes Next

Cohort analysis reveals whether your growth numbers hide underlying problems. Investors examine retention rates by customer acquisition period. Strong cohorts show consistent retention and expansion over time. Weak cohorts indicate product market fit issues, no matter how impressive your headline growth looks.

Customer concentration creates a serious risk. If any single customer represents more than 10% of your revenue, expect valuations to get discounted by 20% to 30%. That dependency creates existential risk that investors price heavily. Diversified customer bases support premium multiples.

Market positioning determines whether your success is sustainable long-term. Investors assess your competitive advantages, switching costs, and network effects. A commodity product in a crowded market commands lower multiples regardless of your current Rule of 40 performance.

Bottom line: the Rule of 40 starts the conversation. Smart investors use it to understand your growth efficiency, then they dig deep into unit economics, market dynamics, and execution capability before they decide what your company is actually worth.

Results vary by company stage and growth trajectory. Companies under $15M ARR may have different investor expectations.

The Questions Everyone Asks

What is the Rule of 40 in simple terms?

The Rule of 40 says your SaaS company’s revenue growth rate plus profit margin should add up to at least 40%. So if you’re growing 30% annually and keeping 10% EBITDA margins, your score is 40%. Investors use this as a quick way to see if you’re balancing growth with profitability effectively. It’s basically a health checkup that takes two minutes instead of two days.

Can a SaaS company succeed with a score below 40%?

Absolutely, especially if you’re still below $5 million in ARR. The Rule of 40 really applies to mature SaaS businesses with established revenue streams. That said, once you’re above $25 million in ARR and consistently scoring below 40%, you’ll face real valuation challenges and limited investor interest unless you have compelling strategic advantages.

Which matters more for valuation: growth rate or profit margin?

It depends on market conditions, but right now in 2025, investors favor balanced growth over hypergrowth at any cost. Growth typically carries more weight in valuations, though companies with Net Revenue Retention above 120% and gross margins above 80% command premium multiples regardless of their Rule of 40 scores. The ideal approach combines 25% to 35% growth with steadily improving profitability.

How do public and private SaaS valuations differ?

Public SaaS companies trade at a median of six to seven times revenue compared to private companies at a median of 4.1 times revenue in 2025. But both markets reward Rule of 40 performance proportionally. Public companies exceeding the benchmark trade at eight to twelve times revenue. Private companies achieving 40% or higher scores can command seven to ten times multiples during acquisitions, which is nearly double the market median. The pattern holds regardless of whether you’re public or private.

When should my company start tracking this metric?

Brad Feld recommends starting when you hit $1 million in monthly recurring revenue, which translates to $12 million in ARR. At that stage, you’ve typically built out your core departments and can meaningfully track operational efficiency. Before that point, just focus on product market fit and initial growth. Obsessing over the Rule of 40 too early is like worrying about your marathon time when you’re still learning to run.

Let’s Talk About Your Company’s Real Value

Understanding what is the Rule of 40 is just the beginning. Whether you’re preparing for your next funding round, considering an exit, or simply want to optimize for maximum value, having the right guidance makes an enormous difference.

Bookman Capital specializes in helping software companies position themselves for optimal valuations. They focus on improving the specific metrics that matter most to investors, from strategic growth planning to profitability optimization. Their team has guided numerous SaaS founders through successful exits, and they understand the nuances that separate good outcomes from exceptional ones.

Don’t leave millions on the table because you didn’t optimize the right metrics at the right time. Schedule a confidential consultation with Bookman Capital to discover your company’s estimated valuation based on current performance, specific strategies to improve your score and command premium multiples, and market timing insights that could significantly impact your exit.

Visit Bookman Capital to learn how their proven approach has helped SaaS companies increase exit valuations by 30% to 50% through strategic metric optimization. Your company’s best exit starts with understanding your numbers, and the team at Bookman Capital knows exactly how to translate those numbers into maximum value.

Sources: