If you’ve ever compared notes with another founder and realized you both hit the same startup revenue milestone, yet walked away with wildly different 409A valuations, you’re not alone. It feels counterintuitive. But once you understand how the process works under the hood, it makes complete sense.

A 409A valuation isn’t a reward for hitting a sales number. It’s an independent assessment of what your common stock is worth right now, today, given everything going on around it. Revenue is part of that picture. It’s just not the whole picture. Not even close.

What Determines a 409A Valuation Beyond Startup Revenue?

The IRS requires private companies to get an independent, third-party appraisal before granting stock options to employees. This appraisal sets the strike price, which is the price employees pay to buy shares. Get it wrong, and both the company and its employees face serious tax consequences.

The valuation firm is building a model of your company’s future, including its growth potential, its risks, and how much of the company’s value will flow to common stockholders when the day comes to cash out. Revenue feeds into that model, but it doesn’t run it.

Think of it this way: startup revenue is the engine size. Two cars can have the same engine. One’s a race car on an open highway. The other’s stuck in gridlock. Their value is completely different, even though the horsepower is identical. The appraiser’s job is to figure out which road your company is on.

The Factors That Move the Needle

Growth Rate: The Single Biggest Differentiator

This is where two companies with identical startup revenue can start to diverge dramatically. Picture this: Company A and Company B both have $2 million in annual recurring revenue. Company A is growing at 200% year-over-year. Company B is growing at 15%.

Their valuations won’t be close. Not even in the same ballpark.

Why? Growth is a signal. It tells the valuation team a story about demand, scalability, and momentum. The income-approach models they run project future cash flows and discount them back to present value. Exponential growth produces a fundamentally different number than modest growth.

One important caveat: sustainable growth matters more than a one-time spike. The appraiser wants to see a clear, repeatable trajectory, not a single quarter that inflated the chart.

Unit Economics: The “How Efficient Is This?” Test

Startup revenue is the top line. But the bottom line matters just as much, and everything in between. Here’s what the valuation firm weighs:

- Gross margin. A SaaS company with 85-90% gross margins is inherently more valuable than a hardware company with 35-40% margins at the same revenue. More of every dollar stays in the business.

- CAC payback period. How many months does it take to earn back the cost of acquiring a customer? A 12-month payback signals a healthier, less risky business than a 36-month payback.

- Burn rate and runway. A company with 24 months of cash runway has more breathing room to execute. That stability directly supports a higher 409A value.

The takeaway: valuations reward capital-efficient businesses. If your unit economics tell a story of sustainable profitability, it shows.

Market Position and Competitive Moats

No startup exists in isolation. Your 409A value is shaped by where you sit in the broader landscape and how durable that position is.

A few market-level factors shape this:

- Total addressable market (TAM). A $100 billion market supports higher growth projections than a $1 billion market. More room to run means more upside in the model.

- Competitive defensibility. A patented technology or strong network effects create a moat. A crowded, feature-race market creates risk. Lower risk commands a higher valuation.

- Industry multiples. Public market comps set the benchmark. If publicly traded SaaS companies are trading at 10x revenue, that number matters. If the industry is struggling and multiples have compressed to 2x, private valuations get dragged down with them.

These external factors don’t just amplify your startup revenue. They answer the deeper question: how likely is this growth to continue?

The Liquidation Stack: The Factor Most Founders Forget

This one is technical, but it might be the most important factor on this entire list. And it’s the reason two companies with identical startup revenue can end up with dramatically different 409A outcomes.

Here’s the core issue: a 409A values common stock, which is the stock held by founders and employees. But common stock sits at the bottom of the payment hierarchy. In a company exit, preferred stockholders (your investors) get paid first.

The more money sitting ahead of common stock in line, and the more aggressive the terms, the less common stock is worth today.

| Startup A (Higher 409A) | Startup B (Lower 409A) | |

| Total Capital Raised | $5 million | $50 million |

| Liquidation Preferences | 1x, non-participating | 2x, participating |

| Preferred Stock Structure | Single series | Multiple stacked series (A, B, C, D) |

| Result | Less investor money to repay first. More exit proceeds flow to common. | Large investor claims with aggressive terms get paid first. Little may be left for common. |

A startup that’s raised $50 million across multiple rounds with participating preferences can have a lower 409A value for common stock than a lean startup that’s only raised $5 million on simple terms, even if they’re pulling in the same revenue. The risk of common stock being “out of the money” in an exit is simply higher.

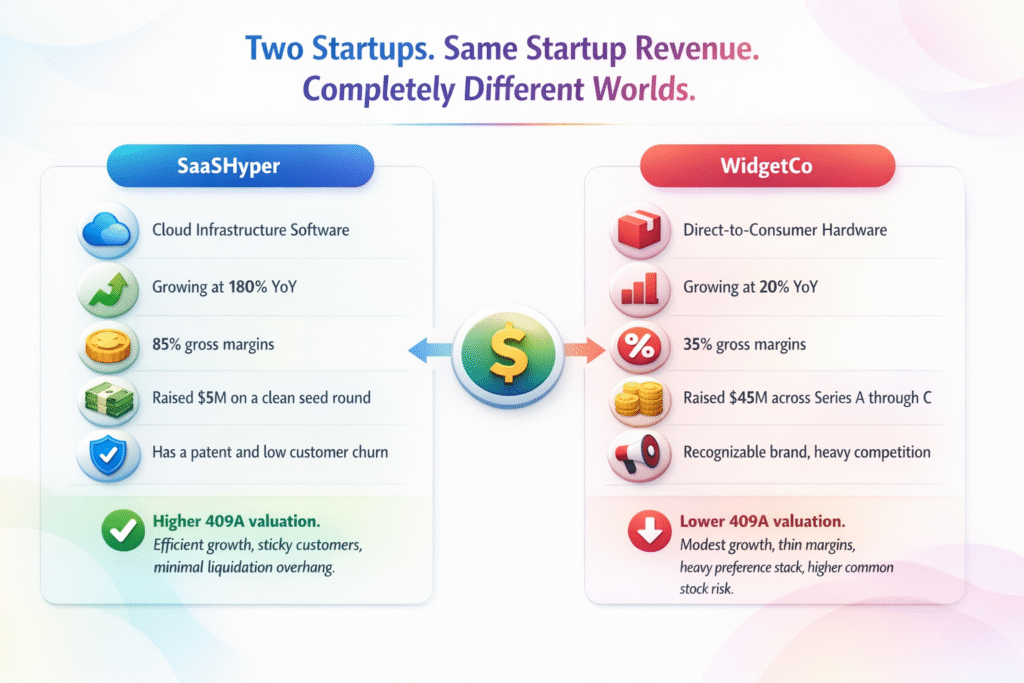

Two Startups. Same Revenue. Very Different Outcomes.

Let’s bring this to life with a simplified, illustrative side-by-side example: two fictional companies, each generating $2M in ARR this year, yet arriving at very different 409A valuations.

SaaSHyper | Cloud Infrastructure Software Growing at 180% year-over-year with 85% gross margins. Raised $5M on a clean seed round. Has a patent and low customer churn. Result: a higher 409A valuation. The numbers tell a strong story: efficient growth, sticky customers, and minimal liquidation overhang.

WidgetCo | Direct-to-Consumer Hardware Growing at 20% year-over-year with 35% gross margins. Raised $45M across Series A through C, with 2x participating preferences. Has a recognizable brand, but faces heavy competition. Result: a lower 409A valuation. Modest growth, thin margins, and a heavy preference stack all increase risk for common stockholders. Future cash flows get discounted more aggressively.

Same startup revenue. Completely different financial stories. The 409A captures that divergence exactly the way it should.

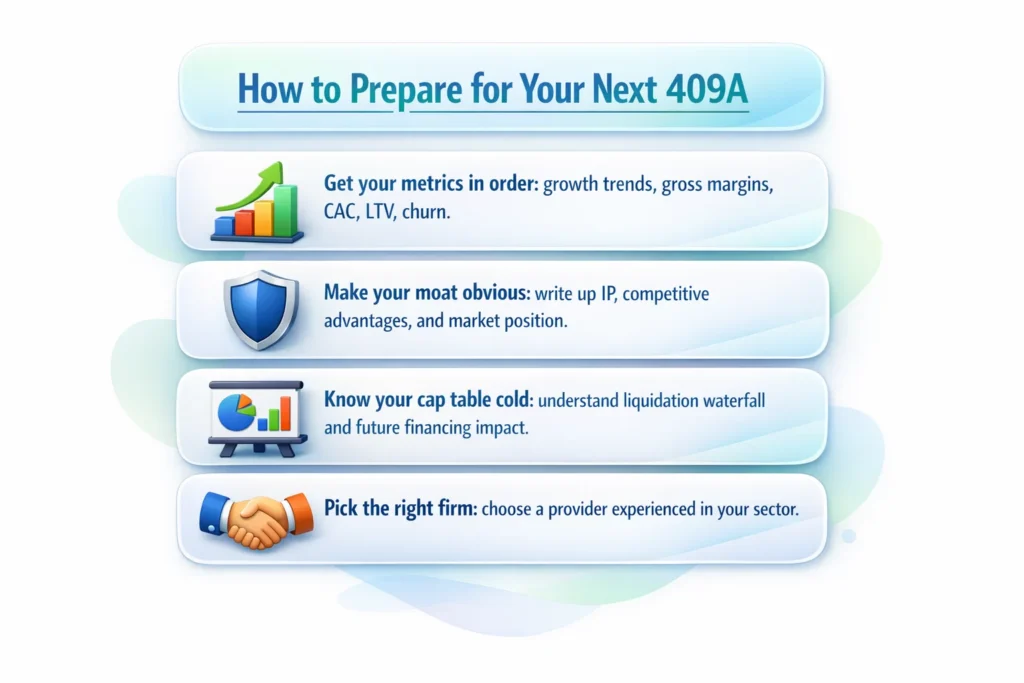

How to Prepare for Your Next 409A (And Make It Work for You)

You can’t argue with an appraiser’s methodology. But you can make sure they have everything they need to tell your company’s full story. Here’s how to prepare smart:

- Get your metrics in order. Pull together clean data on growth trends, gross margins, CAC, LTV, and churn. Don’t leave the appraiser guessing about the quality of your revenue.

- Make your moat obvious. Write up a brief on your IP, competitive advantages, and market position. Even if it feels self-evident to you, don’t assume the appraiser will connect the dots on their own.

- Know your cap table cold. Understand your liquidation waterfall. Be ready to walk through how future financing might affect common stock value. This is where a lot of founders get caught off guard.

- Pick the right firm. Work with a provider that has experience in your sector. They’ll understand your business model and know which public-market comparables apply.

One thing to keep in mind: the goal isn’t the lowest possible number. It’s the most defensible one. An artificially low 409A creates tax headaches down the road for your employees. A well-supported, reasonable valuation is a sign of a healthy company.

Common Questions Founders Ask

Why does our 409A seem so much lower than our last funding round price?

Preferred stock, which is what investors buy, comes with rights and protections that common stock doesn’t have. Liquidation preferences, anti-dilution clauses, and other terms make preferred stock genuinely more valuable per share. On top of that, the valuation process applies discounts for lack of marketability and control. You might hear people say common stock should be “X percent of preferred.” That used to be a back-of-the-napkin rule, but it’s outdated. The actual ratio depends entirely on your company’s specific cap table, preference stack, and stage. There is no reliable benchmark you can apply across companies, which is exactly why the independent appraisal exists.

Can we just use our preferred stock price as the strike price?

No. The IRS explicitly requires an independent 409A valuation to qualify for safe harbor protection. Using your preferred price without a proper appraisal puts both the company and its employees at serious risk of tax penalties.

How often do we need a new 409A?

At minimum, every 12 months. But you also need a fresh valuation after any material event, such as a new funding round, a significant shift in revenue or performance, or an acquisition offer. Missing one of these triggers can void your safe harbor protection entirely.

What happens if our 409A turns out to be wrong?

If the IRS determines the valuation was too low, it can reclassify option gains as wages. That means immediate taxation on all vested options for affected employees, plus a 20% penalty tax and interest on unpaid amounts. The company can also face reporting obligations and reputational risk during audits or an IPO. A qualified, independent appraisal is what protects you. That’s the whole point of safe harbor.

What This Means for Your 409A

Your company is more than a revenue number, and your 409A valuation should reflect that. Growth trajectory, unit economics, market position, and capital structure all shape what your common stock is worth today. Understanding these factors doesn’t just help you make sense of your valuation. It helps you build a company that investors, future employees, and auditors can all feel confident about.

Get a 409A Valuation That Understands Your Story

A 409A valuation should do more than check a compliance box. It should capture your company’s real growth story, efficiency, and potential, and translate that into a number that’s both defensible and fair.

At Bookman Capital, that’s exactly what we do. We provide the rigorous, independent analysis the IRS requires and the clarity your team deserves. If you’re wondering why your valuation is what it is, or want to make sure your next one tells the full story, start with a conversation.

Contact Bookman Capital today.

Sources: