Nobody throws a party when the down market hits.You watch your inbox fill with panic from investors. Your cap table looks less impressive than it did six months ago. Then the 409A valuation lands, and it confirms what you already feared: the number is lower.

Most founders react the same way. They feel like they got punched in the gut. They worry employees will think the company is failing. They wonder if they should hide the news or spin it somehow.

Here is the truth: that lower number is a gift. You just have to know how to open it.

What a 409A Valuation Actually Measures

Let’s clear up the confusion first. A 409A valuation is not your company’s report card. It is not a prediction of your future exit price. It is not what investors would pay for you today.

The 409A valuation is an IRS compliance tool. It determines the fair market value of your common stock. That number sets the strike price for employee stock options. That is its only job.

A Quick Note on History

Congress created Section 409A through the American Jobs Creation Act of 2004, effective January 1, 2005. This was in direct response to Enron executives who accelerated payments under their deferred compensation plans to avoid taxes.

The IRS subsequently issued the implementing regulations. The rule requires that options be priced at or above fair market value on the grant date. Nothing more. Nothing less.

So when your 409A drops, it does not mean your team got worse. It does not mean your product failed. It means the appraiser looked at public market comparables and saw multiple compression across the sector. Tech stocks are trading lower. Your 409A follows suit.

Why “Flat” or “Down” Beats “Up” Every Time

Here is where the mental shift happens. You want your investor valuation to go up. You want your 409A to stay flat or even go down.

Why? Because you grant options to employees at the 409A price. That is what employees pay to buy their shares. A lower strike price means cheaper options for your team.

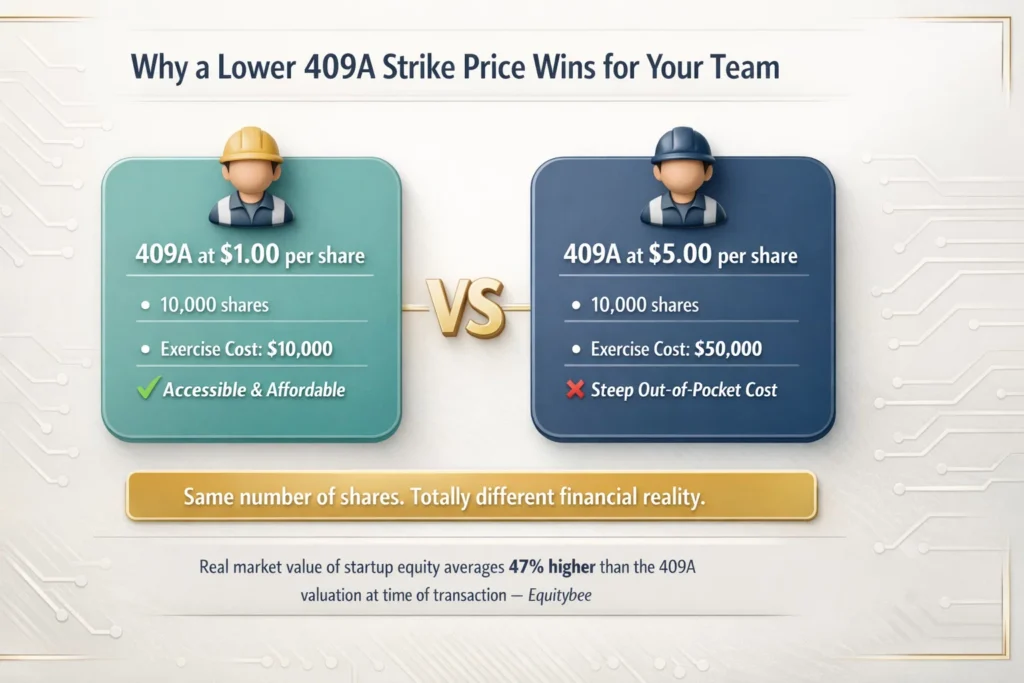

Think about what that does for your culture. A new engineer joins today. She gets options to buy 10,000 shares.

With a 409A at $1.00 per share, she needs $10,000 to exercise. If your 409A were $5.00, she would need $50,000. Same number of shares. Totally different financial reality for her.

According to data from Equitybee, the real market value of startup equity averages 47% higher than the 409A valuation at the time of transaction. That delta is pure potential upside for employees. They buy low and hopefully sell high later.

A down market widens that gap. Your 409A drops with the public comps, but your long-term potential stays intact if you keep executing.

Three Ways a Lower 409A Helps You Win

1. Better Deals for New Hires

Recruiting is brutal right now. Top candidates have options. They look at your offer and compare it to the next startup or even big tech salaries.

A lower strike price makes your equity package more attractive. The potential upside feels bigger because the entry cost is smaller. You can say: “Join us now while the strike price is low.”

That is a real recruiting edge when everyone else is still clinging to their 2021 valuations.

2. Tax Advantages for Everyone

Lower valuations create tax wins. When employees exercise options, they pay taxes on the spread between the strike price and the current fair market value. If the 409A is low, that spread shrinks or even disappears at exercise.

Some founders are also using this moment for estate planning. Gifting equity at a lower valuation can allow you to transfer shares into trusts and reduce future estate tax exposure. This is a strategy worth discussing with a qualified estate attorney.

The federal estate tax rate reaches up to 40%. Locking in a lower valuation on a transfer can matter significantly.

Keep in mind that a 409A report alone is typically not sufficient for gift or estate tax filings. A separate qualified appraisal is usually required.

3. Cheaper Options for the Same Equity Grants

When your 409A is lower, employees pay less per share to exercise their options.

For employees with fixed option grants, this directly reduces their out-of-pocket exercise cost. It shrinks the taxable spread at exercise. This is a real, concrete financial benefit that shows up when it matters most.

What the 409A Does Not See

The valuation process has real blind spots. Appraisers examine your financial statements. They check your cash position. They run comparables against public companies. They may conduct a discounted cash flow analysis.

But the methodology cannot measure everything.

Heidi Roizen of Threshold Ventures has spoken publicly about this limitation. Much of what makes a company truly valuable simply isn’t captured by the 409A process. Team quality, founder vision, and disruptive potential all fall outside the framework.

The framework was designed to prevent tax abuse, not to accurately price a company’s upside.

When the number drops, a lot of what actually drives your long-term value was never in the calculation to begin with. Your culture. Your R&D pipeline. Your unfair advantages in the market.

Material Events That Trigger a New Valuation

You cannot run one 409A and forget it. The rules require updates whenever material changes occur. Here is what forces a fresh look:

| Trigger Event | Why It Matters |

| New financing round | Preferred stock price changes the valuation inputs |

| 12 months elapsed | Safe harbor protection expires automatically |

| Major customer win or loss | Revenue projections shift materially |

| Product launch | Changes the company’s risk and growth profile |

| Secondary stock sales | New transaction data becomes available |

| Acquisition talks | Material non-public information now exists |

Most startups schedule annual valuations. But if something significant happens mid-cycle, don’t wait.

Granting options on an expired valuation breaks the safe harbor. Employees then face a 20% additional IRS penalty on top of regular income taxes. That gets ugly fast.

The Investor Perspective You Forgot

Founders worry what VCs will think. If our 409A dropped, will they lose confidence?

Experienced investors understand 409A mechanics. They know the valuation serves tax purposes, not market pricing. They actually prefer that founders follow safe harbor rules. It signals governance sophistication.

Sloppy compliance creates liability. Good governance impresses buyers later.

Some investors even expect the 409A to lag behind the preferred price. That gap exists by design. Preferred stock carries extra rights and liquidation preferences. Common stock lacks those features, so it gets a discount.

Your Series A lead paid $5.00 per share for preferred. Your 409A might come in at $2.50 for common. That does not mean the company halved in value. It means the appraiser properly accounted for the structural differences between share classes.

How to Talk About This With Your Team

Employees hear “valuation drop” and think “company trouble.” You need to lead them through the logic. Do not hide the number. Do not pretend it did not happen.

Explain what a 409A actually does. Tell them it sets their strike price. Show them how a lower strike directly benefits their personal finances at exercise.

One founder framed it this way for her team: “This is like putting a discount tag on something you wanted to buy anyway. You still get it. You just pay less.”

Walk them through the inputs. Public comps fell. Those factors moved the number. None of that changes the mission or the market opportunity you’re all working toward.

Be honest. Be clear. Your team will appreciate the transparency.

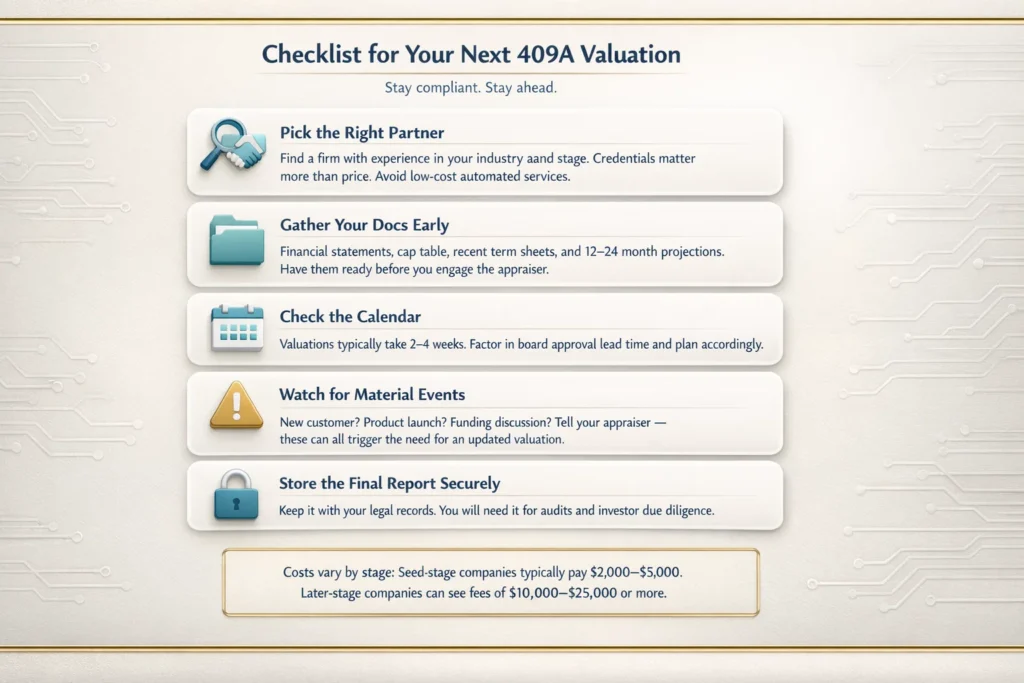

Checklist for Your Next 409A

Getting ready for a valuation does not have to hurt. Follow this list and stay ahead of the game.

Pick the right partner. Find a firm with experience in your industry and stage. Credentials matter more than price. Avoid low-cost automated services that may not withstand IRS scrutiny.

Gather your docs early. Financial statements, cap table, recent term sheets, and 12 to 24 month projections. Have them ready before you engage the appraiser.

Check the calendar. Valuations typically take 2 to 4 weeks. Factor in board approval lead time and plan accordingly.

Watch for material events. New customer? Product launch? Funding discussion? Tell your appraiser. These can all trigger the need for an updated valuation.

Store the final report securely. Keep it with your legal records. You will need it for audits and investor due diligence.

Costs vary by stage and complexity. Seed-stage companies typically pay $2,000 to $5,000. Later-stage companies with complex capital structures can see fees of $10,000 to $25,000 or more. It’s worth every dollar for the safe harbor protection it provides.

The Math of a Down Market

In 2022, Stripe and Instacart saw their internal valuations cut by 28% and 38%, respectively, following new 409A appraisals. The headlines screamed trouble.

But inside those companies, employees who received new option grants got cheaper strike prices. This was a direct, tangible benefit tied to the same market forces driving the headlines.

Public SaaS companies that once traded at 10x revenue compressed to 7x or lower. That multiple compression flows through to every 409A in the sector. Your execution did not cause the drop. The market did.

So stop treating a flat or down 409A like bad news. It is not a verdict on your company. It is a tax rule doing its job. And right now, that rule is working in your team’s favor.

Your Next Move

You have options to grant. Talent to hire. A mission to execute. The market will do what it does. You cannot control the comps or the multiples. You can control how you use this moment.

A lower 409A means cheaper options for your team, better recruiting conversations., and tax advantages that smart founders are locking in right now. Don’t waste it.

At Bookman Capital, we help founders navigate the difference between investor value and 409A value. We know how to structure equity to win in any market.

Contact Bookman Capital today. Let us build the strategy that turns today’s flat valuation into tomorrow’s wealth. Your team is waiting. Your future self will thank you.

Sources: