Fintech grows by moving money, moving data, or moving risk. Regulators set the boundaries for those moves. A 409A valuation sits on assumptions that describe risk, timing, and outcomes as of a specific valuation date.

Regulatory risk changes what the company can do, where it can do it, and how much it costs to do it. Those changes flow into revenue timing, margins, and the chance of reaching a liquidity event. Appraisers then translate that operating reality into fair market value for common stock.

What fintech regulatory risk means in valuation language

Regulatory risk describes the chance that a legal requirement changes business operations. The requirement can show up as a licensing gate, a supervisory exam, or an enforcement action. The operational impact shows up in launch timing, product scope, ongoing controls, and capital needs.

A 409A valuation uses facts and circumstances as of the valuation date. The report treats some regulatory items as material and treats other items as background noise. Materiality depends on how the item changes value drivers in a measurable way.

The oversight areas fintech leaders run into most

Fintech oversight depends on activity and structure. Payments and stored value often trigger licensing questions. Lending triggers consumer disclosure and servicing questions. Investing and custody models trigger securities and custody questions.

Anti-money laundering obligations also depend on coverage status. Coverage depends on whether the business qualifies as a regulated financial institution category, such as a money services business under FinCEN rules.

The 409A foundations that regulation touches

A 409A valuation for private company stock uses a reasonable valuation method applied reasonably. The regulation points to factors such as tangible and intangible assets, anticipated cash flows, comparable companies, and recent arm’s-length transactions, with a focus on information that materially affects value.

The same ruleset also warns against stale inputs. A prior calculation becomes unreasonable on a later date when it fails to reflect later available information that materially affects value. The text gives examples like resolving material litigation or issuing a patent, and it also flags the case where the prior valuation date is more than 12 months earlier than the date when the valuation is used.

Regulatory facts fit inside that “material information” frame. A license approval changes the geographic scope. A formal exam finding can change cost and continuity risk.

How regulatory risk changes 409A assumptions

Regulatory risk does not map into valuation math in one automatic step. Appraisers apply judgment when they quantify risk and when they decide whether to quantify it separately from broader business risk. That discretion varies across firms and engagement scopes.

Even with that nuance, the direction stays consistent. Constraints that delay revenue reduce present value. Constraints that increase cost reduce margins. Constraints that raise continuity risk increase risk adjustments.

The assumption set that gets adjusted first

Regulatory posture most often affects a short list of model inputs.

- Revenue start date

- Revenue growth rate by geography or product line

- Gross margin through compliance spend and dispute losses

- Operating expense through compliance headcount, vendors, and audits

- Working capital needs through reserves and settlement timing

- Probability of a successful financing round

- Time to liquidity for IPO or acquisition paths

- Discount rate inputs that reflect business risk and time risk

Appraisers treat these as assumptions, not as facts. The fact sits in the evidence package, and then the appraiser interprets the fact and chooses an input.

The safe harbor point that founders often miss

People use “safe harbor” because it just sounds nice. The regulation describes a presumption of reasonableness for certain valuation methods, and the Commissioner can rebut the presumption only by showing that the method or its application was grossly unreasonable. That standard shifts the dispute burden and raises the bar for the IRS challenge.

The safe harbor concept also includes three recognized paths in the regulation’s presumption list.

The three IRS-recognized safe harbor valuation methods

The regulation lists these three methods under the presumption of reasonableness section.

- Independent appraisal within 12 months

The method uses an independent appraisal meeting specified requirements and dated no more than 12 months before the relevant transaction. - The binding formula valuation is used consistently

The method uses a formula valuation that qualifies under the rule, and the company uses it consistently for covered transfers, with stated exceptions. - Illiquid startup valuation in good faith with a written report

The method values illiquid stock of a startup corporation using a reasonable, good-faith process supported by a written report that considers relevant factors, with eligibility limits such as no material trade or business for 10 years or more, and restrictions when a near-term change in control or public offering is reasonably anticipated.Safe harbor does not erase the need for accuracy. Safe harbor changes the fight posture if a challenge shows up.

The real stakes for employees and the company

Mispriced equity can trigger painful tax outcomes under Section 409A. The statute describes income inclusion for certain failures, plus interest, plus an additional tax equal to 20 percent of the compensation required to be included in gross income.

This risk matters in fintech because regulatory events can move valuation inputs fast. Option grants that happen after a material change need a valuation story that matches the new facts. The costs land on people, not just on a spreadsheet.

Regulatory risk to valuation math: the chain, with the missing nuance

A clean story helps, and a fake clean story hurts. Regulatory facts do not automatically force a specific discount rate bump. Regulatory facts change operating constraints, and the appraiser decides whether the change is material and how to quantify it.

A dated license approval is a fact. A dated exam finding is a fact. The valuation effect comes from interpretation, with explicit reasoning in the report.

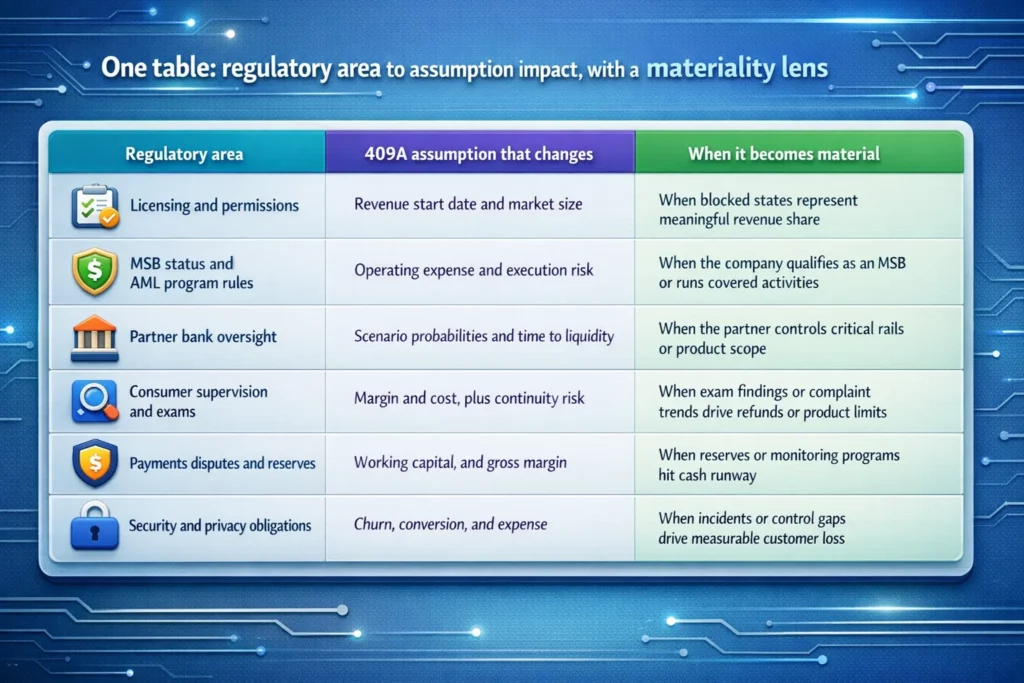

The regulatory issues that most often move 409A assumptions

10 issues that drive material changes in fintech valuation inputs

- Licensing coverage and licensing gaps

Licensing status limits legal operating geography. Geographic limits shift revenue timing and market size assumptions. - Bank partner dependency and contract control points

Partner contracts can impose approval gates for products and pricing. Termination rights and program controls raise continuity risk. - BSA and AML program obligations when the business qualifies as covered

Money services businesses face program requirements under FinCEN rules. Coverage depends on the business meeting MSB definitions and triggers, so not every fintech lands here. - Identity checks and onboarding friction

Customer identification steps affect funnel conversion. Higher friction increases customer acquisition cost per active user. - Sanctions screening and alert operations

Screening tools generate alerts and reviews. Review backlogs, slow transaction speed, and raise support costs. - Consumer complaint handling and disclosure accuracy

Complaint volume drives staffing and refunds. Disclosure changes can force rework in product flows and servicing. - Payments dispute rates and network monitoring programs

High disputes can lead to reserves or monitoring pressure from networks or partners. Reserves tie up cash and change working capital assumptions. - Data security incidents and remediation work

Incidents create response costs and remediation costs. Incidents can also reduce customer trust and increase churn. - Lending compliance and governance overhead

Lending products require disclosure steps and adverse action style notices in many contexts. Governance adds time and adds operating expense. - Securities and custody posture for investing products

Registration and custody structure affect product scope. Structure decisions can change the timeline for launch and scale.

Each issue becomes material only when it moves a key value driver. Appraisers apply that materiality filter in the facts and circumstances frame.

What appraisers actually do with regulatory facts

Different appraisal firms request different inputs. Some firms ask for deep compliance evidence. Some firms rely more on management representations when risk stays low, and the engagement scope stays narrow.

A practical rule still holds. The company lowers valuation friction when it backs claims with dated documents and metrics.

12 evidence items that usually strengthen regulatory assumptions

- State licensing map with approval dates and pending applications

- Bank partner agreement and program governance exhibits

- Compliance policy set with version dates and owner roles

- Independent review or audit outputs for relevant control programs

- Training logs and completion rates for covered staff

- Identity and onboarding funnel metrics by month

- Alert volumes and closure time metrics for monitoring workflows

- Complaint logs and resolution time metrics

- Chargeback and dispute ratios by month for payment products

- Reserve notices or settlement timing documentation when reserves apply

- Incident reports and remediation tracking for security events

- Legal and regulatory correspondence tied to key events

This list supports the idea of verifiability without claiming one universal standard. Appraisers still decide what they need, and the company can still steer the engagement with a clean packet.

The table keeps the chain honest. It treats materiality as a filter, not as an afterthought.

When a regulatory change triggers a 409A refresh

A valuation stays reasonable when it reflects all available information material to value. A valuation also becomes questionable when it relies on a prior calculation that does not reflect later material information.

Regulatory events land in the “later material information” bucket when they change scope, timing, or cost measurably. A license approval that unlocks major states can qualify. A formal remediation requirement that adds cost can qualify.

The clean move is procedural. Update the fact set. Align board minutes, forecasts, and grant dates.

Your next option grant should not guess at compliance risk

Fintech teams can run fast without getting sloppy. The team can log regulatory events with dates. The team can track the funnel and dispute metrics monthly. The team can keep partner controls visible, not buried.

This approach makes the valuation more defensible. It also lowers the chance that employees face nasty surprises under Section 409A’s income inclusion, interest, and 20 percent additional tax rules.

Talk to Bookman Capital about a fintech 409A that matches real oversight

Bookman Capital supports fintech teams that operate with licensing constraints, partner oversight, and real compliance costs. The engagement ties regulatory facts to valuation assumptions with a written, dated logic trail that stands up in audits and board review.

Contact Bookman Capital today.

Sources:

- U.S. Treasury regulations for Section 409A, including reasonable valuation method concepts

https://www.law.cornell.edu/cfr/text/26/1.409A-1 (Legal Information Institute) - U.S. eCFR rules for money services businesses, including AML program requirements

https://www.ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1022 (eCFR) - CFPB supervision and examinations page and the Supervision and Examination Manual entry point

https://www.consumerfinance.gov/compliance/supervision-examinations/ (Consumer Financial Protection Bureau)