Property valuation sets the value of real estate as of a specific date. Banks require it for loans. Buyers use it to avoid overpaying, and sellers use it to price with proof. Investors use it to size risk, returns, and exit options.

Market value follows a standard definition in valuation standards. Market value describes a sale between a willing buyer and a willing seller, at arm’s length, after proper marketing, with both parties acting knowledgeably and without compulsion. That definition sets the rules for how a value opinion must read.

Appraisers rely on three main appraisal approaches in formal reports. Investors and developers also use two extra methods because speed and feasibility matter in real deals. This guide covers five methods of property valuation, with inputs, best-fit uses, and limits.

What a valuation method means in practice

A valuation method uses a repeatable process with measurable inputs. Those inputs include sales prices, construction costs, and property income. The method produces a value opinion for a defined purpose, such as lending, buying, insurance, or development.

Appraisers document sources and assumptions. Lenders expect that documentation, and so do courts and tax authorities. Clear evidence keeps the valuation defensible.

Method 1: Sales comparison approach

The sales comparison approach estimates value by comparing the subject property to similar properties that sold recently. Appraisers analyze location, size, condition, age, and features. Then they adjust comparable sale prices to match the subject.

This approach mirrors buyer behavior. Buyers compare alternatives and react to recent closed sales. The method reflects what the market paid, not what someone hoped to get.

How appraisers run it

Appraisers select comparable sales with similar utility and appeal. They verify sale terms when reliable records exist, because distressed terms can distort the price. They apply adjustments for differences that buyers pay for in that market.

Typical adjustment buckets include:

- Living area and lot size

- Condition and renovation level

- Bedroom and bathroom count

- Parking, storage, and amenity access

- View, noise, and location factors

The final value comes from reconciling adjusted indications. One strong comparable can outweigh several weak ones.

Best-fit properties

This approach fits residential property in active markets. It also fits small multifamily properties when enough similar sales exist. Lenders prefer it for single-family home lending because it aligns with market evidence. For 2–4 unit properties, lenders typically require the income approach alongside it.

Method 2: Cost approach

The cost approach estimates value from what it costs to build an equivalent structure today. The method adds land value, then subtracts depreciation from the improvements. It works well when the building stays new, unusual, or hard to match with sales.

It answers a blunt question. What does it cost to replace the building on this site as of today?

The standard structure

Property value follows a consistent structure:

- Property value equals land value plus replacement cost new minus depreciation.

- Land value comes from land sales, supported allocation, or other accepted land techniques.

- Replacement cost new comes from cost services, contractor estimates, and local cost data.

Replacement cost means a modern equivalent, not a replica of every detail. That difference affects older properties with outdated materials.

Depreciation categories used in reports

Depreciation represents a measurable loss in value from the improvement.

- Physical deterioration reflects wear, damage, and age.

- Functional obsolescence reflects design limits, such as poor layout or low ceiling height.

- External obsolescence reflects outside impacts, such as traffic noise or nearby industrial activity.

Appraisers support depreciation with observed condition and market evidence. Numbers without support do not hold up in review.

Best-fit properties

The cost approach fits new construction. It fits special purpose properties, like schools and some medical facilities, where sales data stays limited. Insurers also use cost-based logic to estimate replacement coverage amounts.

Method 3: Income capitalization approach

The income capitalization approach values property based on income production. The method converts net operating income into value using a market-supported capitalization rate. It fits commercial real estate and stabilized rental property.

Income property trades like a business. Cash flow drives the price, and buyers compare returns across alternatives.

Direct capitalization in one line

Direct capitalization uses a simple relationship:

- Value equals net operating income divided by capitalization rate.

Net operating income equals effective gross income minus operating expenses. Operating expenses include management, repairs, insurance, and property taxes. Debt service does not belong in NOI in standard appraisal practice.

Inputs that move the value

This method stands on documented inputs:

- The rent roll and lease terms define the income structure.

- Vacancy and credit loss reduce effective income.

- Expense history supports stabilized operations.

- Market cap rates reflect risk and expected return for comparable assets.

A small change in the cap rate shifts the value quickly. Appraisers support cap rates with comparable sales and market surveys where available.

Best-fit properties

This approach fits apartments, offices, retail, industrial, and mixed-use assets with trackable income. It also fits leased single-tenant properties when lease terms and credit quality stay clear. Banks rely on it for income-producing collateral because income supports debt.

Method 4: Gross rent multiplier method

The gross rent multiplier method estimates value using gross rental income. The method compares sale price to gross annual rent, then applies a market multiplier to similar rentals.

Investors use GRM because it moves quickly. It flags deals that look overpriced before deeper underwriting starts. It does not replace a full income analysis, and it does not pretend to.

What GRM uses and what it ignores

GRM uses gross rent. GRM ignores operating expenses. GRM also ignores vacancy differences unless the rent figure already reflects effective rent.

That gap matters. Two buildings can earn the same gross rent, yet one produces a stronger NOI because expenses stay lower.

Best-fit properties

GRM fits small rental properties with consistent market rent data. It fits duplexes, small multifamily, and simple rentals in the same submarket. It works best when investors compare like-for-like properties in the same neighborhood.

Method 5: Residual method

The residual method estimates land value from development feasibility math. The method starts with the expected value of the completed project. Then it subtracts all development costs and the required developer profit.

The remainder equals residual land value. Developers use that number to set a maximum land offer, and then negotiations start from there.

Common cost categories included

Residual calculations include documented cost lines:

- Construction and site works

- Professional fees, permits, and inspections

- Financing costs, interest, and lender fees

- Marketing and sales costs

- Contingency allowances

- Developer profit requirement

Inputs come from plans, zoning rules, market pricing, and credible cost estimates. A weak assumption breaks the result, so cost and value support matter.

Best-fit properties

The residual method fits vacant land. It fits major renovations and change of use projects. It also fits mixed-use development planning, where the end value depends on the final unit mix.

Which method fits which job

| Valuation method | Primary purpose | Primary inputs | Best-fit property types |

| Sales comparison approach | Market value for typical assets | Comparable closed sales and adjustments | Homes, condos, small multifamily |

| Cost approach | Replacement value and limited comp support | Land value, replacement cost, depreciation | New builds, special purpose assets |

| Income capitalization approach | Value from cash flow | NOI, cap rate, rent roll, expenses | Commercial and stabilized rentals |

| Gross rent multiplier method | Fast rental screening | Gross annual rent, market GRM | Small rentals in the same submarket |

| Residual method | Development land value and feasibility | Completed value, costs, required profit | Land, redevelopment, mixed use plans |

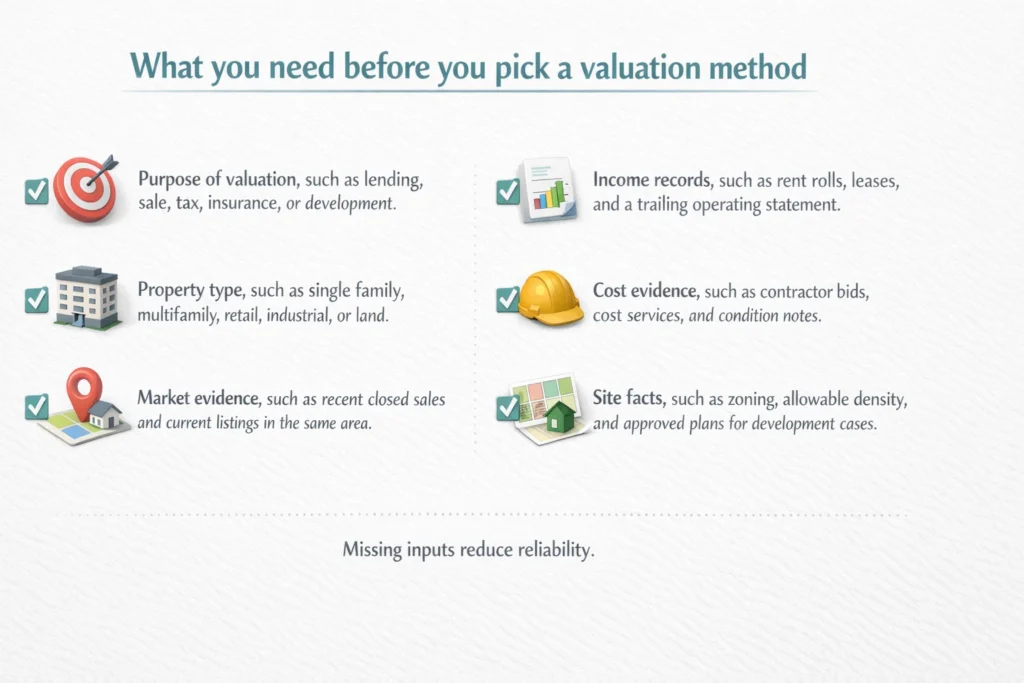

What you need before you pick a valuation method

- Purpose of valuation, such as lending, sale, tax, insurance, or development.

- Property type, such as single-family, multifamily, retail, industrial, or land.

- Market evidence, such as recent closed sales and current listings in the same area.

- Income records, such as rent rolls, leases, and a trailing operating statement.

- Cost evidence, such as contractor bids, cost services, and condition notes.

- Site facts, such as zoning, allowable density, and approved plans for development cases.

Weak data produces a wider value range, and that affects pricing and lending.

How professionals reconcile results when methods disagree

A valuation report can include more than one method. The appraiser weighs methods based on relevance and data quality. Then the appraiser explains that weighting in the reconciliation section.

A tract home often points to sales comparison as the strongest evidence. A new special-purpose building often points to the cost approach. A leased retail property often points to the income approach because rent and risk drive price.

FAQ

1) What are the main appraisal approaches to property valuation?

The main appraisal approaches include the sales comparison approach, the cost approach, and the income capitalization approach. Formal appraisal education and valuation standards commonly present these three as the primary approaches.

2) What method works best for rental properties?

Rental property valuation often uses the income capitalization approach because net operating income drives value. Investors also use the gross rent multiplier method for quick screening before they review expenses and vacancy.

3) What is the difference between GRM and cap rate?

GRM uses gross rent and ignores operating expenses. Cap rate uses net operating income, so it reflects operating expenses and vacancy in the value calculation.

4) When does the residual method matter most?

The residual method matters when land value depends on future development value. The method supports feasibility decisions and maximum bid pricing for land and redevelopment.

Connect your property valuation to a clear financing plan

Bookman Capital helps align valuation with real financing decisions. The team reviews the valuation method, key inputs, and risk drivers, then shapes funding terms around verified market support. Stabilized rentals tie to NOI and cap rates. Redevelopment deals are tied to residual land value and cost evidence. For lending or investment discussions built on defensible valuation, contact Bookman Capital at https://bookmancapital.io/.

Sources: