Who needs estate valuation and who performs estate valuation are two of the first questions families ask when an estate needs accurate asset values.

That question matters early. Executors need values to inventory property, report assets, pay debts, and distribute what remains. The IRS says a personal representative collects assets, pays creditors, files tax returns, and distributes property to heirs or beneficiaries.

Heirs need values too. The reported value affects the basis in inherited property. The IRS says inherited property generally takes a basis equal to fair market value on the date of death, unless a different rule applies.

Courts also need values. Probate filings rely on an inventory that shows what the estate owns and what those assets are worth. California probate procedure, for example, requires an inventory and appraisal in decedents’ estates.

This article stays on that one issue. It explains who needs estate valuation, who performs it, and how those people work together.

The people who needs estate valuation first

Estate valuation is not one person’s problem. Several groups need it for different reasons.

Executors and administrators need an estate valuation to run the estate

The executor or administrator usually needs an estate valuation first. That person has to identify property, collect records, deal with creditors, and prepare the estate for filings and distribution. Each step depends on supported values.

The rule can stretch wider when no formal executor is acting. The IRS states that, for estate tax purposes, the term “executor” includes anyone in actual or constructive possession of any property of the decedent if no executor is appointed, qualified, and acting within the United States.

That matters in real life. Families still need numbers even when court paperwork moves slowly.

Heirs and beneficiaries need an estate valuation to understand what they receive

Heirs need estate valuation because value affects what they inherit on paper and what tax basis they take later. If an heir sells inherited real estate or stock, basis helps determine gain or loss. The IRS ties inherited basis to fair market value on the date of death in most cases.

So, estate valuation does more than support probate. It also sets the starting number for later tax reporting.

Probate courts need an estate valuation to review the estate record

Probate courts need values because they review inventories, appraisals, and other estate filings. Courts do not work from rough guesses. They expect a clear record that shows what the estate owns and what those assets are worth.

That record keeps disputes down. It also gives the court a usable picture of the estate.

Tax authorities need an estate valuation when a return is required

Tax authorities need an estate valuation when a federal estate tax return is required. The IRS instructions for Form 706 state that property is generally valued as of the date of death, unless the executor elects alternate valuation under section 2032.

That rule is direct. The estate must match its numbers to the right valuation date.

A quick list of the people who need estate valuation

Here is the first listicle.

- Executors and administrators need values to inventory property, file returns, pay debts, and distribute assets.

- Heirs and beneficiaries need values to understand the inherited basis and future sale reporting.

- Probate courts need values to review estate inventories and appraisals.

- Tax authorities need values when estate tax reporting rules apply.

- Trustees and fiduciaries need values when they account for estate-related assets under their control. That duty follows the same need for accurate records and proper administration.

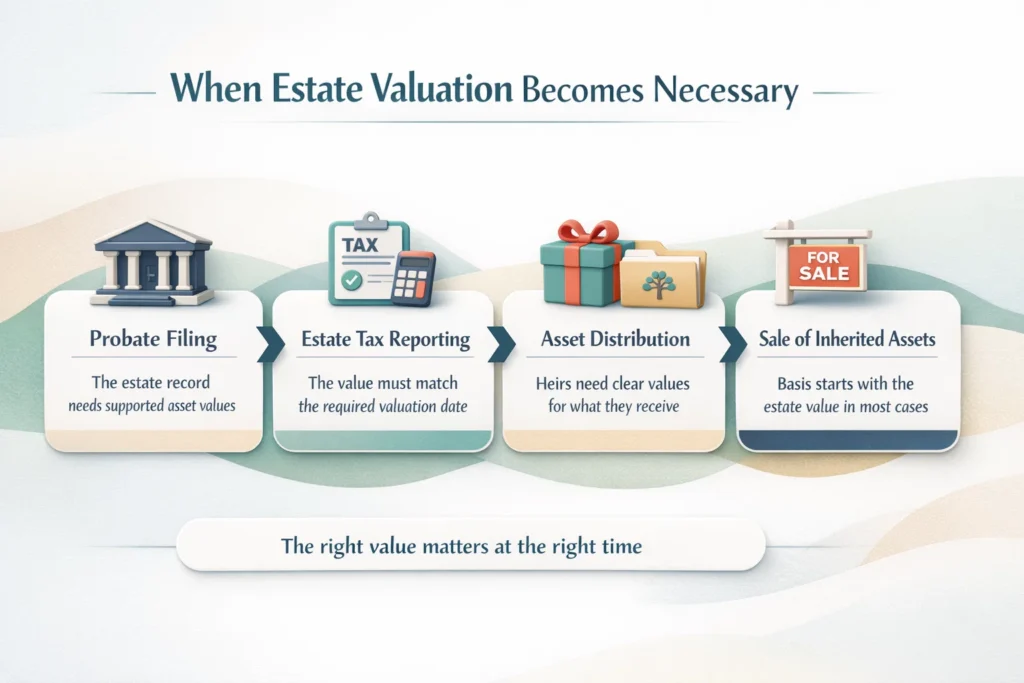

When estate valuation becomes necessary

Timing matters because the estate has to use the right value on the right date.

Probate triggers the need for supported values

Probate often triggers the need first. Once the estate opens, the representative has to identify property and prepare the estate record. Courts and estate professionals then rely on those values in later steps.

Tax reporting adds a second layer

Tax reporting can add another layer of urgency. The IRS uses the date of death value as the general rule for estate tax valuation, unless the estate elects alternate valuation where the law allows it.

That election changes timing, not the need for support. The estate still needs real evidence for each figure.

Distribution and later asset sales keep the numbers relevant

Distribution does not end the value question. Heirs may need the estate value later when they sell inherited assets or review estate records. The original valuation keeps doing work after the estate closes.

Who actually performs estate valuation?

The executor manages the process, but specialists often perform the valuation work. Different assets call for different experts. That is the clean answer.

Real estate appraisers value land and buildings

Real estate appraisers usually value homes, land, rental property, and commercial buildings. They study the property, review market data, and report an opinion of value for the required date. The Appraisal Foundation states that USPAP serves as the generally recognized ethical and performance standard for the appraisal profession in the United States.

Personal property appraisers value items people can move or collect

Personal property appraisers work on art, jewelry, antiques, collections, and similar items. The IRS explains that a qualified appraiser needs verifiable education and experience in valuing the type of property at issue.

That asset-specific rule matters. A person who values houses does not automatically qualify to value fine art.

Business valuation professionals value private business interests

Closely held business interests usually require a business valuation professional. The IRS instructions for Form 706 direct the filer to attach appraisals for certain property, and IRS estate tax examination guidance for closely held businesses discusses review of the appraisal, ownership records, financial information, transfer restrictions, and buy-sell agreements when those documents affect value.

This area gets technical fast. Ownership terms and transfer limits can change value.

Probate referees or court-accepted appraisers value assets in some states

Some states use court-linked appraisal systems for parts of the estate process. California probate practice gives one clear example through the Inventory and Appraisal process.

That system does not replace every outside expert. It does show that court practice can shape who performs the work.

The second listicle: who performs estate valuation by asset type

- Real estate appraisers value houses, land, and commercial property.

- Personal property appraisers value art, antiques, jewelry, and collectibles.

- Business valuation professionals value private company interests and related ownership rights.

- Probate referees or court-accepted appraisers value assets where state procedure uses that system.

- Financial institutions and market records help establish values for publicly traded securities and account balances on the correct date.

- Executors and personal representatives gather records, hire specialists, and place the supported values into estate filings.

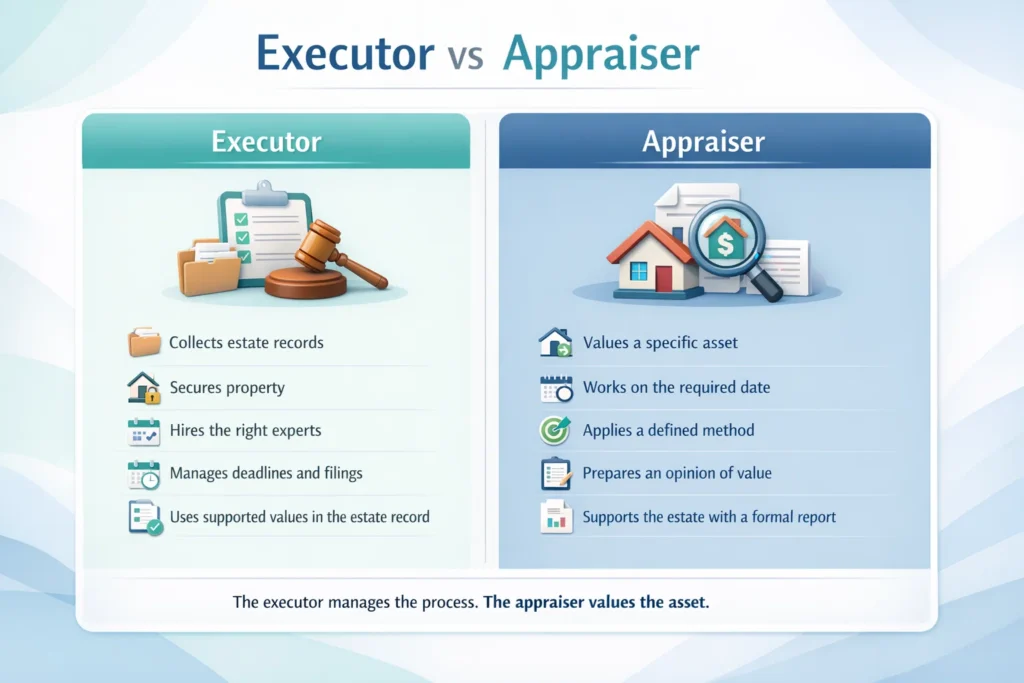

What the executor does and what the appraiser does

People lump these roles together. They are different jobs.

The executor manages records, deadlines, and filings

The executor gathers information, secures property, hires the right experts, and keeps the estate moving. The IRS describes the personal representative’s duty to collect assets, pay debts, file returns, and distribute property.

The executor does not need to value every asset personally. The executor needs to obtain and use supported values.

The appraiser values a defined asset on a defined date

The appraiser studies a specific asset and produces an opinion of value. That work ties to a property type and a valuation date. It also follows professional standards in the relevant appraisal field.

The attorney and tax adviser support the legal and tax side

The attorney handles probate procedures and legal filings. The tax adviser handles return preparation and tax reporting. Those roles support the estate, but they do not replace asset-specific valuation experts when the estate needs them.

A simple table that shows who needs the valuation and who does the work

| Party | Why do they need an estate valuation | Who usually performs the valuation |

| Executor or administrator | To inventory assets, file returns, pay debts, and distribute property | The executor coordinates. Asset-specific appraisers provide opinions of value. |

| Heir or beneficiary | To understand the inherited basis and the value of the distributed property | The estate obtains the valuation. Heirs rely on the final estate records. |

| Probate court | To review inventories and appraisals | The court-accepted appraisers, probate referees, or qualified outside valuers |

| IRS or tax preparer | To report date-based estate values when required | Qualified appraisers, market records, and estate filings |

| Trustee or fiduciary | To account for assets under administration | The fiduciary coordinates. Asset-specific valuers support the record. |

What makes a person qualified to perform estate valuation?

Qualification depends on the asset, not just the title on a business card.

Asset-specific experience matters

The IRS says a qualified appraiser must have verifiable education and experience in valuing the type of property being appraised.

That rule cuts through the noise. The right appraiser has to know the actual asset class.

Professional standards matter too

The Appraisal Foundation states that USPAP sets the generally recognized ethical and performance standard for the appraisal profession in the United States.

Standards matter because estate valuation needs support, a method, and a clear reporting date.

Independence matters when the estate faces review

IRS examination guidance for closely held businesses discusses the review of the independence and qualifications of the appraiser.

That is a practical warning. A weak report can invite trouble.

Need a clear path for the assets that are hardest to value?

Estate valuation gets easier when each asset goes to the right expert from the start. Real estate, private business interests, collectibles, and financial accounts do not follow the same playbook. Bookman Capital helps families, executors, and fiduciaries sort out what needs valuation and who should handle it, with a clear process that keeps the estate moving.

If you want help identifying the right valuation approach for your estate assets, contact Bookman Capital at https://bookmancapital.io/contact/.

Sources: