The 409A valuation and tax valuation serve two completely different purposes in business finance. You hear “valuation” and think taxes. That’s fair. But in the wild world of startups and equity, two different animals use the same name. We’re talking about the 409A valuation and the standard tax valuation.

They seem like twins from a distance. Up close, they serve totally different masters. One keeps the IRS happy for stock options. The other settles a score for the taxman on a property or business sale. Mixing them up creates expensive compliance problems. Let’s pull these concepts apart.

The Core Mission: What Each Valuation Actually Does

Every valuation has a job. The purpose defines the process. You wouldn’t use a butter knife to cut down a tree. Same idea here.

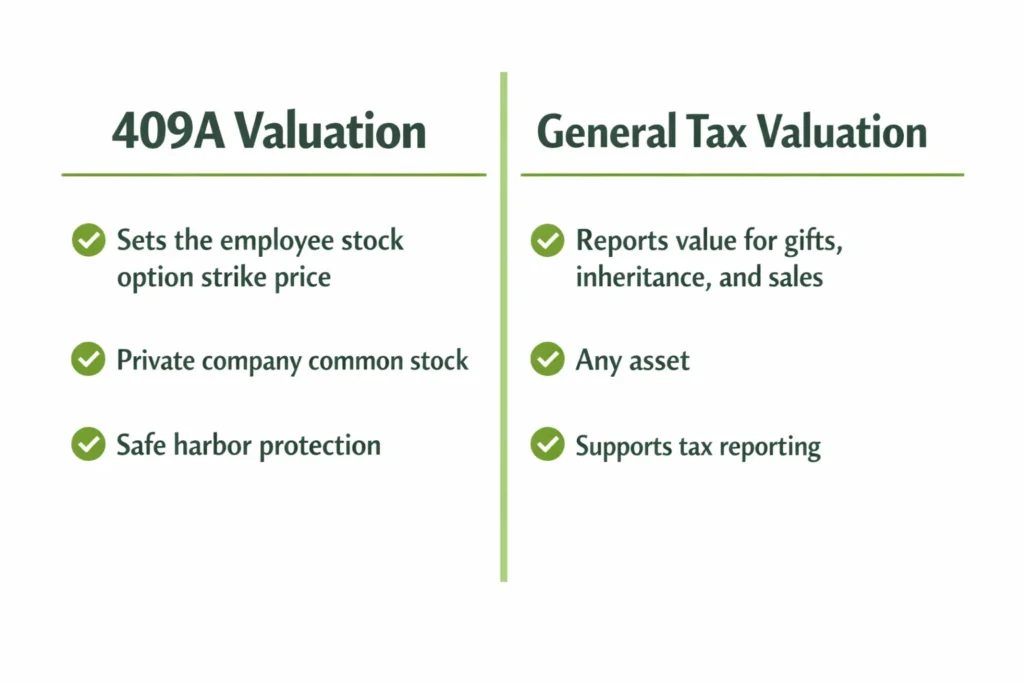

A 409A valuation finds the fair market value of your company’s common stock. It’s a specific, regulated process. The Internal Revenue Service created it under Section 409A of the tax code, enacted as part of the American Jobs Creation Act of 2004. This number sets the strike price for employee stock options. The goal is to avoid punitive taxes for your team. It answers one question: What is one share of our common stock worth right now?

A general tax valuation determines the value of an asset for federal tax purposes. This is a much broader category. It applies to things like gifted family business shares, inherited real estate, or a sold partnership interest. The goal is to report an accurate value to the IRS for a transaction. It answers: What was this specific asset worth on this specific date for this tax form?

The Report Card: How the IRS Judges Each One

The IRS reviews both types of valuations. Their grading rubric, however, changes completely. This is where the distinction gets concrete.

For a 409A valuation, the IRS demands a specific methodology under Treasury Regulations. The valuation must follow accepted business valuation approaches and be performed by qualified appraisers to achieve “safe harbor” status, which shifts the burden of proof to the IRS if the valuation is challenged.

Independent, qualified appraisers typically perform this work. The report defends the fair market value of the common stock. It often applies discounts for lack of control and marketability. This reflects the restricted nature of employee shares.

The IRS wants to ensure companies do not grant options with an unfairly low strike price.

For a general tax valuation, the IRS follows general valuation principles across various asset classes. According to IRS guidelines, fair market value is defined as “the price that property would sell for on the open market…between a willing buyer and a willing seller, neither being required to act, and both having reasonable knowledge of the relevant facts.”

Appraisers use accepted methods for the specific asset class. The appraisal report must withstand IRS scrutiny and potential audit. The focus is on the accurate reporting of asset transfer taxes.

Key Difference at a Glance

| Feature | 409A Valuation | General Tax Valuation |

| Governing Rule | IRS Section 409A | IRS Tax Code (Various Sections) |

| Primary Purpose | Sets the employee stock option strike price | Reports value for gifts, inheritance, and sales |

| Asset Valued | Private company common stock | Any asset (real estate, business, art, etc.) |

| Critical Output | Fair Market Value (FMV) per share | Fair Market Value of the entire asset |

| Typical Discounts | Lack of Control, Lack of Marketability | Varies by asset type |

The Process Showdown: Building the Numbers

How do appraisers even arrive at these numbers? The engines under the hood use similar fuel but are tuned for different races.

For a 409A, the process is standardized for startups. Appraisers analyze the company’s financials. They review the capital structure and outstanding shares.

The market approach and income approach are common. The Backsolve Method, which uses recent preferred stock prices, is frequently used for funded companies. The report is a technical document. It includes a detailed conclusion of value for the common stock.

For a deeper understanding of how appraisers select and apply different valuation methodologies based on your company’s specific situation, see our comprehensive guide at How Appraisers Determine 409A Valuations.

For a tax valuation, the process depends on the asset. Valuing a commercial building involves comparing recent property sales. Valuing a family business might involve analyzing its cash flows.

The appraiser selects the most appropriate valuation methods. They gather comparable data and apply necessary premiums or discounts. The report justifies the final value for the IRS.

Two Major Lists of Reasons You Need Them

List 1: You Need a 409A Valuation When…

- You plan to grant stock options to employees or advisors.

- Your company’s last 409A is over 12 months old.

- You experience a material event like a new funding round.

- You need a safe harbor from IRS penalties for your team.

List 2: You Need a General Tax Valuation When…

- You gift shares of a private business to a family member.

- You are filing an estate tax return after an inheritance.

- You donate a high-value asset to a charity.

- You are resolving a dispute with the IRS over asset value.

The Cost of Confusion: Real-World Consequences

Using the wrong valuation type has direct penalties. The IRS does not accept excuses.

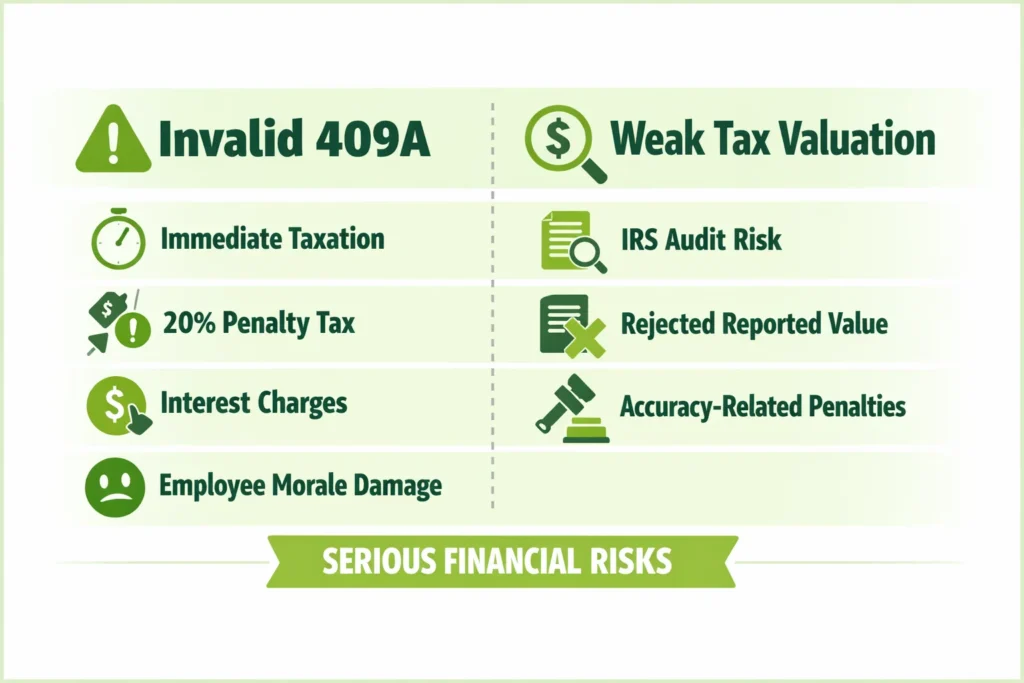

If you use an invalid 409A, your employees face trouble. According to Section 409A of the Internal Revenue Code, their stock options gain non-qualified status. All deferred compensation becomes taxable immediately.

Recipients pay income tax plus a 20% penalty tax. Interest charges also apply. This devastates employee morale and creates legal liability.

If you use a weak tax valuation, you risk an audit. The IRS can reject your reported asset value. They can impose additional taxes.

They can add accuracy-related penalties. These penalties are typically 20% of the underpaid tax. The process becomes stressful and costly.

Frequently Asked Questions

Can one appraisal serve both purposes? Almost never. The 409A values only common stock for a specific IRS rule. A tax valuation targets a different asset for a different tax form.

The scopes and objectives mismatch completely. Using one for the other fails IRS requirements.

How often do I need a new 409A valuation? According to IRS safe harbor requirements, you need a fresh 409A valuation at least every 12 months to maintain compliance.

You also need one after a material event. Material events include new financing rounds, acquisitions, significant changes in financial performance, or other events that could materially affect your company’s value.

Think of it as an annual tune-up with extra check-ups for big life events.

Does the IRS pre-approve these valuations? No, the IRS does not pre-approve any valuation.

For 409A, using an independent, qualified appraiser creates a “safe harbor.” Under safe harbor protection, the IRS must prove your valuation was “grossly unreasonable” rather than requiring you to defend its accuracy. This safe harbor shifts the burden of proof to the IRS during an audit.

For tax valuations, a credible appraisal report is your primary defense.

What makes a valuation “qualified” for the IRS safe harbor? To qualify for safe harbor status, the valuation must be conducted by a qualified, independent third-party appraiser following generally accepted appraisal practices.

The appraiser must have relevant experience and credentials. The valuation firm must be independent from the company. The process must follow accepted valuation principles.

The report must be comprehensive and well-documented. It’s not just a number on a page.

Getting the Right Tool for the Job

This stuff is complicated, but the takeaway is simple. A 409A valuation is a specific, recurring tool for pricing stock options. A general tax valuation is a broader tool for reporting asset transfers. They are both tax valuations in the widest sense, but they are not interchangeable. Using the wrong one costs real money and creates real headaches.

Your company needs the correct valuation to protect itself and your team. You need expertise that understands the exact IRS rules for your situation. You need clarity, not guesswork.

Bookman Capital provides precise 409A valuations for startups and precise tax valuations for asset transfers. We give you the right report for the right job, full stop. Contact Bookman Capital at https://bookmancapital.io/ to start a conversation. Let’s get your equity or asset taxes handled right.

Sources: