Late-stage startups assume valuation discipline becomes automatic once scale arrives, but that assumption often proves wrong. In practice, poor 409A timing creates larger consequences at this stage than it did in the early years.

As the company grows, equity volume increases, capital events accelerate, and audit scrutiny intensifies. At the same time, board expectations rise and investor oversight strengthens, so equity grants often move faster than valuation updates.

When a 409A valuation update lags behind a material event, the exposure spreads quickly and affects more employees and more value than founders expect.

Growth Multiplies Exposure, Not Protection

Late-stage startups issue equity frequently. New hire grants, executive packages, and refresh awards depend on the current fair market value.

A 409A valuation determines the fair market value of common stock. The board uses that value to set stock option strike prices.

When valuation timing lags business events, strike prices disconnect from current company facts. Scale magnifies the impact.

What 409A Timing Actually Controls

409A timing controls whether a valuation reflects known information on the grant date. Material information includes financing rounds, revenue acceleration, acquisitions, and structural changes.

A valuation older than twelve months does not qualify for safe harbor reliance. A valuation can become unreasonable earlier if material events occur.

Late-stage companies experience material events frequently. Timing discipline must match operational speed.

The Twelve-Month Rule Is Often Misunderstood

Many teams repeat one phrase. A 409A valuation lasts twelve months.

That phrase applies only when no material change occurs. A priced financing round qualifies as new material information.

Rapid revenue growth changes projected cash flows. Acquisitions alter the asset base and earnings outlook. Each event requires a valuation review. The calendar does not override a material change.

Where Late-Stage Startups Feel the Consequences

Timing errors surface during formal review periods. Operations may not detect them immediately.

Audit Season

Auditors examine stock-based compensation under ASC 718. They compare grant dates with valuation dates.

If grants follow material events without updated valuations, auditors question reasonableness. Documentation becomes critical.

IPO Preparation

Underwriters review capitalization history. Investment banks analyze valuation timing and governance records. Inconsistent strike prices create diligence friction. Friction slows IPO readiness.

M&A Diligence

Acquirers request valuation reports and equity records. Legal teams analyze patterns in grant timing. Inconsistent timing signals process weakness. Process weakness affects negotiation leverage.

Seven Real Consequences of Poor 409A Timing

- Strike prices misalign with company performance

Grants issued after strong growth require updated assumptions. - Audit testing expands in scope

Auditors request additional valuation evidence. - Accounting workload increases

Finance teams defend expense recognition and grant timing. - Board oversight becomes reactive

Directors address corrective steps instead of a strategy. - Employee confidence declines

Perceived inequities in option pricing create internal friction. - Diligence cycles lengthen

Buyers request supplemental analysis and explanation. - Transaction timelines stretch

IPO or acquisition schedules absorb timing review delays.

Each outcome traces back to delayed valuation reassessment.

How Material Events Accumulate in Late-Stage Companies

Late-stage startups operate with momentum. Revenue grows quarter over quarter. Enterprise deals close unexpectedly. Forecast revisions occur midyear.

Secondary liquidity events introduce pricing reference points. New investors alter preferred share terms. These developments compound quickly. Valuation calendars often trail behind operational reality.

Common Late-Stage 409A Valuation Triggers

Below are events that typically require review or refresh:

- Closing a significant financing round

- Experiencing rapid revenue acceleration

- Completing a transformative acquisition

- Initiating IPO preparation

- Conducting a large secondary transaction

- Changing strategic direction under new leadership

Each trigger affects fair market value assumptions. Each requires a documented evaluation.

Risk Pattern Table for Late-Stage Companies

| Company Event | Why It Affects 409A Valuation | Risk if Not Updated |

| New financing round | Changes the capital structure and investor rights | Strike prices misstate the fair market value |

| Rapid revenue growth | Alters forecast cash flows | Valuation assumptions become outdated |

| Acquisition | Expands earnings and asset base | The allocation model becomes inaccurate |

| Secondary transaction | Introduces pricing reference | Auditor questions valuation timing |

Late-stage startups experience these events often. Valuation timing must follow event timing.

The Compliance Dimension

Section 409A governs deferred compensation rules. Stock options granted below fair market value create tax exposure. The exposure applies directly to employees. Penalties include income acceleration and additional tax.

Companies rely on the independent valuation safe harbor protection. Safe harbor strength depends on timing and reasonableness.

Late-stage valuation errors affect larger equity pools. Financial exposure increases with scale.

What Strong 409A Timing Looks Like

Strong timing requires ownership and process. One executive tracks valuation dates and material triggers.

Finance and legal teams conduct quarterly reviews of material events. Board calendars include valuation checkpoints.

Grant cycles align with valuation refresh cycles. Coordination prevents reactive corrections. Institutional discipline protects enterprise value.

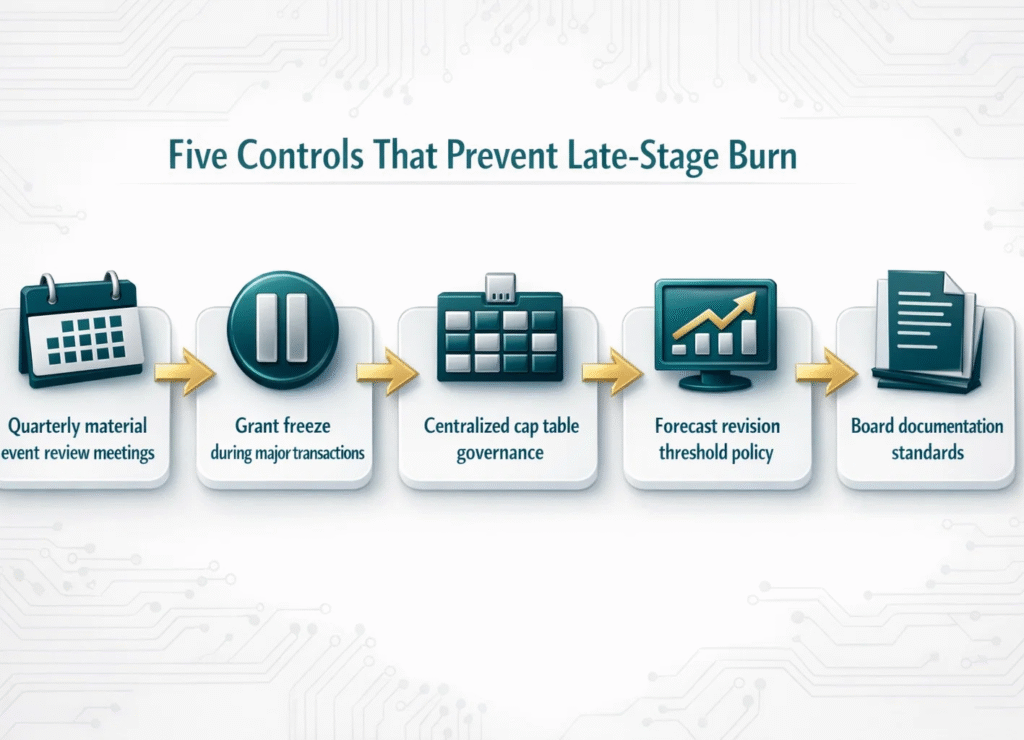

Five Controls That Prevent Late-Stage Burn

- Quarterly material event review meetings

Teams assess new financing, growth, and structural changes formally. - Grant freeze during major transactions

Temporary pauses prevent issuing awards under outdated assumptions. - Centralized cap table governance

A single source of truth reduces input errors. - Forecast revision threshold policy

Significant projection changes trigger valuation reassessment. - Board documentation standards

Minutes clearly record valuation timing decisions.

These controls reduce audit friction and transaction risk.

Frequently Asked Questions

Do late-stage startups need more frequent 409A valuation updates

Yes. Late-stage startups experience frequent material events that require valuation review.

Is a twelve-month valuation always safe?

No. The 12-month rule applies only when no material change affects fair market value assumptions.

What happens if options were granted before updating?

Auditors and counsel evaluate timing. The company may require updated valuation support or corrective documentation.

Does IPO readiness increase scrutiny?

Yes. Underwriters and auditors review valuation timing closely during IPO preparation.

The Business Cost of Getting Timing Wrong

Late-stage startups manage higher valuations and larger option pools. Poor 409A timing increases compliance exposure and transaction friction.

Audit disputes consume executive time. Due diligence delays weaken negotiation leverage.

Equity inconsistency affects employee morale. Each issue stems from preventable timing gaps.

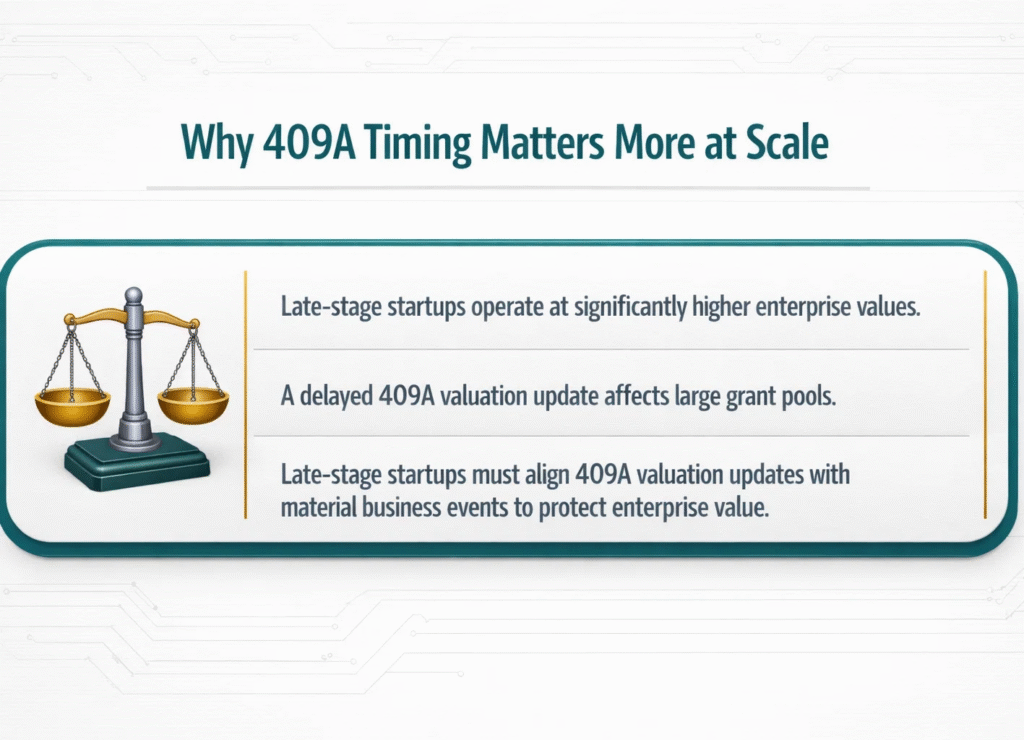

Why 409A Timing Matters More at Scale

Late-stage startups operate at significantly higher enterprise values. A small shift in fair market value can impact millions in equity exposure.

A delayed 409A valuation update affects large grant pools. Hundreds of employees may receive options tied to outdated assumptions.

Late-stage startups also face stronger audit, investor, and IPO scrutiny. Review teams examine valuation timing and stock option pricing closely.

Consistent 409A valuation discipline demonstrates governance maturity. Proper 409A timing protects safe harbor defensibility and employee trust.

As valuation increases, risk increases. Late-stage startups must align 409A valuation updates with material business events to protect enterprise value.

Protect Your Next Milestone with Proper 409A Timing

Late-stage growth raises stakes. A 409A valuation timing must align with business events.

Bookman Capital helps late-stage startups coordinate valuation updates with material milestones and preserve safe harbor defensibility.

Our team ensures that your 409A valuation timing supports your next phase of growth. Contact Bookman Capital Today!

Sources: