Estate assets form the foundation of any will or trust. When a person passes away, everything they owned becomes part of their estate. Getting the numbers right on those estate assets is one of the most critical jobs for an executor. But what happens when those numbers are off?

Slapping a random price tag on a jewelry collection or guessing the value of a stock portfolio can blow up fast. It can mean angry beneficiaries, surprise tax bills, or even legal trouble. This article breaks down the real-world consequences of misvaluing estate assets and shows you how to get it right the first time.

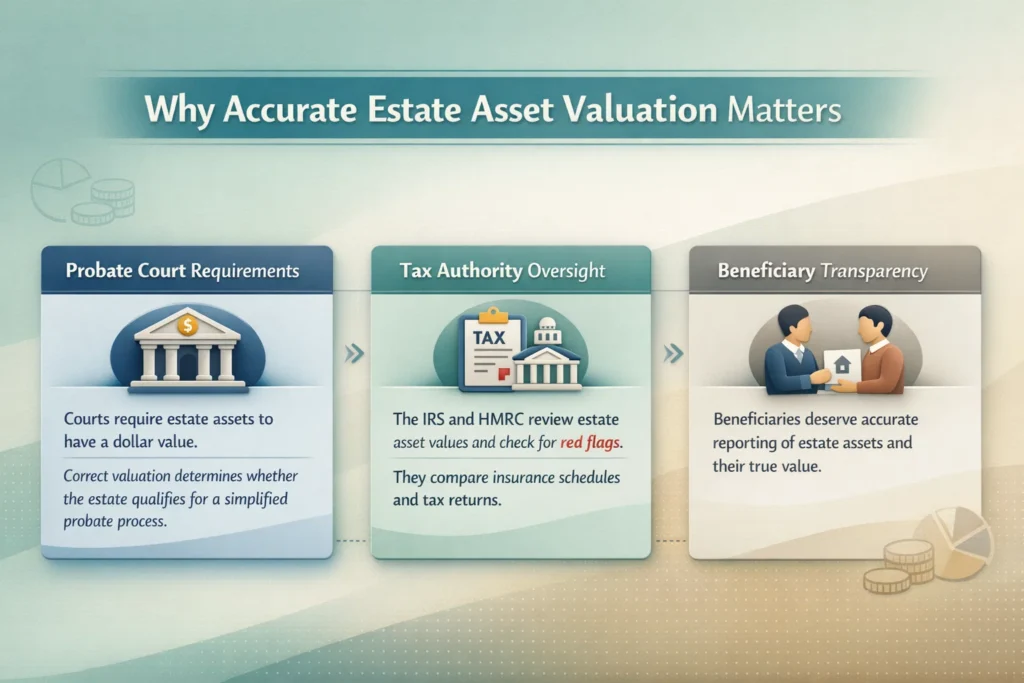

Why Accurate Estate Asset Valuation Matters

The clock starts ticking the moment someone dies. Estate assets need a dollar amount attached to them for several reasons. Courts require it. Tax agencies demand it. Beneficiaries deserve it.

Probate courts use these values to oversee the administration process. If the total value falls under a certain threshold, the estate might qualify for a simplified probate process. Overvalue, and you might go through a longer, costlier process than necessary.

Tax authorities take valuation seriously. The IRS and HMRC both have dedicated teams that check whether estate assets were valued correctly. They look for red flags like insurance values being used instead of fair market value, and they cross-check insurance schedules against tax returns.

What Happens When Estate Assets Are Undervalued?

Skimping on estate asset values seems like a smart way to reduce taxes. It almost never works out well.

Tax Penalties and Interest Charges Arrive Fast

The IRS knows when numbers look off. When the music legend Prince died, the IRS determined the entire estate was undervalued by approximately 50 percent. The administrator reported the estate at $82.3 million while the IRS valued it at $163.2 million. The IRS issued a notice of deficiency for $32.4 million in additional estate taxes plus a separate $6.4 million accuracy-related penalty for substantial undervaluation.

HMRC in the UK can impose penalties up to 100 percent of the extra tax due for a deliberate and concealed error. That means if you underpaid by $50,000, you could owe another $50,000 just in penalties. Even a careless error can trigger penalties of up to 30 percent. Interest keeps accruing the whole time too.

Beneficiaries Face Bigger Capital Gains Tax Later

Undervaluing estate assets creates a nasty surprise when beneficiaries sell inherited property. When someone inherits an asset, they get a “step-up” in cost basis. That means their tax basis becomes the fair market value on the date of death. If that value was set too low, their basis is artificially low too.

The IRS requires executors to file Form 8971 and provide a Schedule A to beneficiaries. Beneficiaries must generally use that value as their basis. Sell that asset later and the capital gain looks huge. A house valued at $200,000 for probate that sells for $250,000 three years later triggers tax on $50,000 of gain. But if the real value at death was $240,000, the actual gain is only $10,000.

Court Battles and Legal Challenges Arise

The Estate of Kollsman v. Commissioner shows what happens when estate assets get undervalued with a compromised appraisal. The estate’s expert reported the two Old Master paintings at $500,000 and $100,000. The court found the expert had a significant conflict of interest because he was simultaneously seeking the right to auction those paintings at Sotheby’s. He also exaggerated the paintings’ dirtiness and failed to use comparable sales data to support his valuations.

The Tax Court sided with the IRS expert and valued the paintings at $1,995,000 and $375,000 respectively. The Ninth Circuit affirmed. The estate paid far more in the end than a proper independent appraisal would have cost.

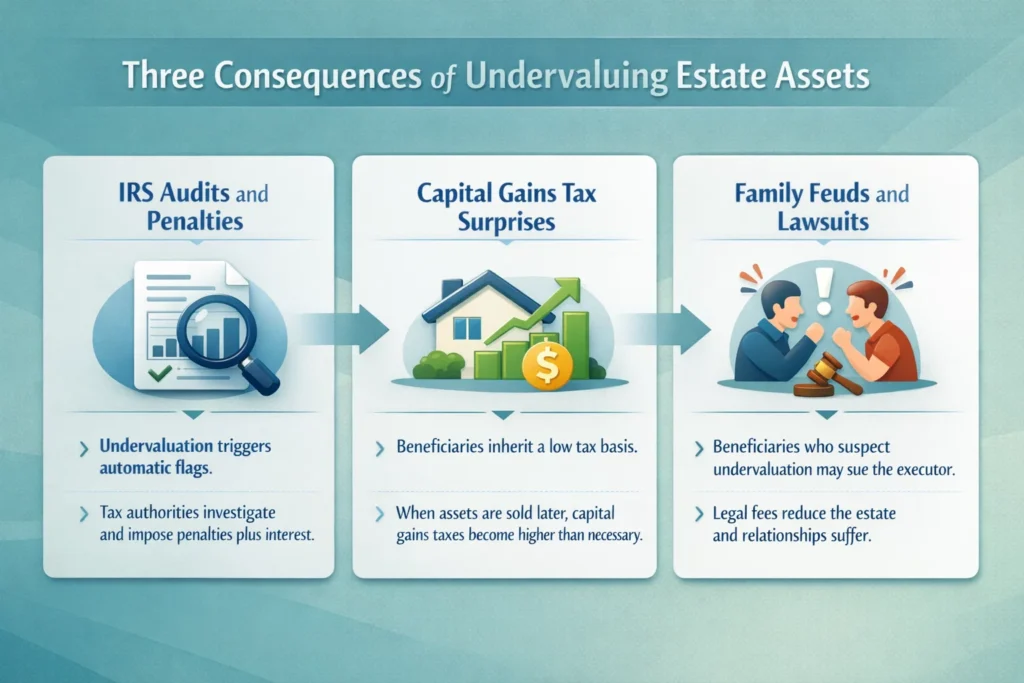

Three Consequences of Undervaluing Estate Assets

- IRS Audits and Penalties: Undervaluation triggers automatic flags. Tax authorities investigate and impose penalties plus interest. The Prince estate faced $32.4 million in additional taxes and a $6.4 million penalty for alleged undervaluation of the whole estate.

- Capital Gains Tax Surprises: Beneficiaries inherit a low tax basis. When they sell inherited assets, they pay more capital gains tax than necessary. A low probate value means a higher tax bill later.

- Family Feuds and Lawsuits: Beneficiaries who suspect assets were undervalued can sue the executor. Legal fees eat into the estate, and relationships get destroyed.

What Happens When Estate Assets Are Overvalued?

Paying too much tax seems impossible, but it happens constantly. Executors overvalue estate assets all the time, often without realizing it.

The Estate Pays Tax That Was Never Due

Overvaluation means the estate pays inheritance or estate tax on money it never actually had. HMRC guidance specifically warns that insurance valuations are not the same as open market value. Yet executors keep using insured values, which are almost always higher than what items would actually sell for.

A dining table insured for £4,000 might sell at auction for £300. Using the £4,000 figure inflates the estate value. That pushes the estate into higher tax brackets or uses up relief it should not touch. The estate cuts a check to the tax authority for money that does not exist in real terms.

Executor Fees and Bond Costs Spike

Probate courts set the amount of the executor’s bond based on estate value. Overvalue the estate and the bond requirement goes up. That means higher premiums paid from estate funds. Money that could go to beneficiaries instead pays for unnecessary insurance.

In some states, statutory fees for executors and attorneys are calculated as a percentage of estate value. Overvaluing estate assets artificially inflates those fees. Beneficiaries get less while professionals get more.

Heirs Expect Money That Does Not Exist

Tell beneficiaries they are inheriting a $50,000 coin collection. They start making plans. Then the collection sells for $15,000 at auction. Now everyone is disappointed and angry. The executor looks incompetent or worse.

Three Consequences of Overvaluing Estate Assets

- Paying Tax That Was Not Due: Insurance values are not market values. Using the wrong number means overpaying inheritance tax. Beneficiaries lose money that should be theirs.

- Higher Professional Fees: Executor and attorney fees based on asset value go up. Bond premiums increase. The estate bleeds cash on unnecessary expenses.

- Broken Promises to Heirs: Beneficiaries expect the values you told them. When assets sell for less, they blame you. Relationships fracture over money that never existed.

How Valuation Errors Impact the Executor Personally

Executors need to understand something crucial: they can be personally liable for mistakes. If the estate does not have enough money to cover extra taxes or penalties, the executor pays out of pocket.

Distributing assets before all taxes are paid is a classic error. If the IRS comes back for more money and the assets are already gone, the executor writes the check personally. A qualified appraiser’s written report provides cover if questions come up later.

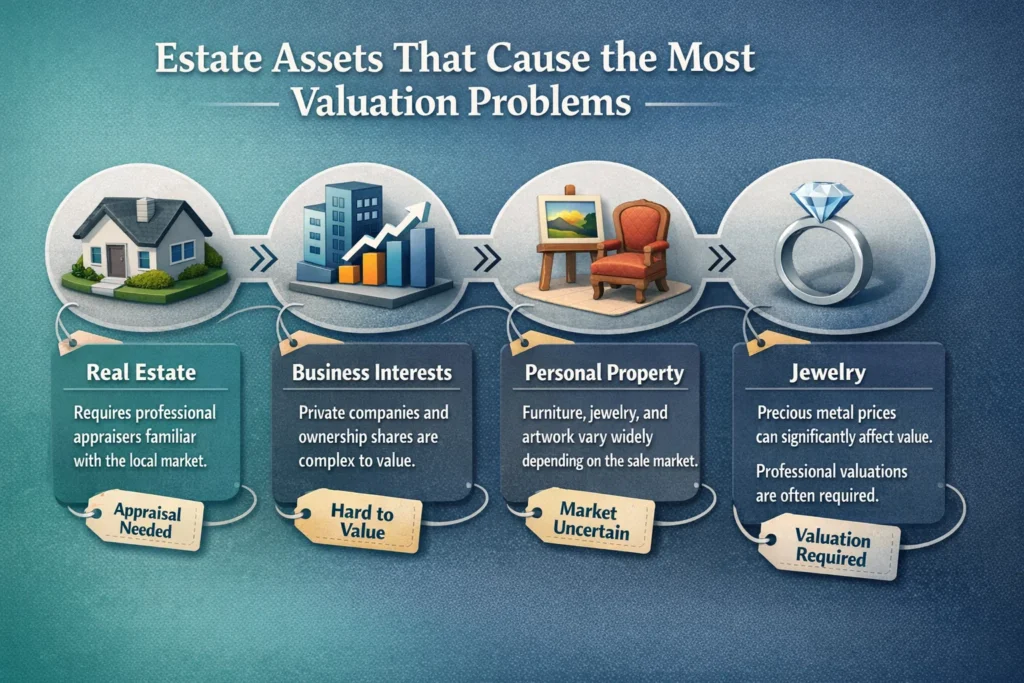

Which Estate Assets Cause the Most Valuation Problems?

Some estate assets cause more problems than others. Real estate looks straightforward but it requires professional appraisers who know the local market. Business interests get complicated fast, especially for private companies.

Personal property causes the most arguments. Furniture, jewelry, and artwork have wildly different values depending on where and how they are sold. Auction market values are usually the gold standard for documentation.

The Palliser v HMRC case shows how development potential must be considered in property valuations. A property valued at approximately £1.24 million for probate based on the deceased’s 88.4% share was sold for £2.525 million less than two years later. After HMRC challenged the valuation, the tribunal settled on approximately £1.6 million as the correct figure for inheritance tax purposes.

Jewelry trips up executors constantly. With precious metal prices at current levels, even simple gold rings can exceed reporting thresholds. In the UK, anything over £1,500 needs an individual listing and a professional valuation.

What Does Proper Estate Asset Valuation Look Like?

The only way to avoid these disasters is proper professional valuation from the start.

Professional appraisers follow strict standards. In the US, the Uniform Standards of Professional Appraisal Practice requires appraisers to certify that they have no financial interest in the property being valued. That certification protects the estate from conflicts of the kind that sank the Kollsman estate.

Good valuations for estate assets must meet specific criteria: they must use the date of death as the valuation date, they must be prepared on an open market value basis, and they must comply with relevant tax laws. Anything less invites trouble.

Comparing Valuation Outcomes

| Valuation Type | Immediate Tax Impact | Future Tax Impact | Legal Risk Level |

| Undervalued | Lower tax bill now | Higher capital gains later | High risk of penalties |

| Overvalued | Higher tax bill now | Lower capital gains later | Medium risk of disputes |

| Accurate Value | Correct tax paid | Correct basis established | Low risk all around |

Do not let a bad appraisal define the estate you are handling. Get the values right. Use qualified independent appraisers. Document everything. Your beneficiaries will thank you and the tax authorities will leave you alone.

Need help navigating estate asset valuations?

The team at Bookman Capital can guide you through the process and connect you with the right professionals. Reach out today before a valuation mistake turns into a tax bill.

Every day you wait is a day the IRS or HMRC gets closer to flagging your numbers. Bookman Capital works with executors and estate administrators who want clean valuations, zero penalties, and beneficiaries who actually trust them. Stop guessing and start getting it right. Contact Bookman Capital now.

Sources:

- Internal Revenue Service (IRS) — About Form 8971, Information Regarding Beneficiaries Acquiring Property from a Decedent Official US government page covering the executor’s obligation to report estate asset values to beneficiaries and the IRS, including the consistent basis reporting requirement under IRC section 1014(f).

- Estate of Kollsman v. Commissioner, No. 18-70565 (9th Cir. 2019) — FindLaw Full text of the Ninth Circuit opinion affirming the Tax Court’s rejection of the estate’s art appraisal due to the expert’s conflict of interest, exaggerated dirtiness claims, and absence of comparable sales data.

- Palliser v Revenue and Customs [2018] UKUT 71 (LC) — rossmartin.co.uk Analysis of the Upper Tribunal (Lands Chamber) decision confirming that hope value and development potential must be factored into probate property valuations for UK inheritance tax purposes under s.160 IHTA 1984.