A retrospective property valuation tells you exactly what a piece of real estate was worth on a specific day in the past. Property markets shift constantly, reacting to economies, interest rates, and broader trends, which is why you cannot simply guess this number or work backward from today’s price.

Think of it as a financial snapshot. A retrospective valuation tells you exactly what a piece of property was worth on a specific day in the past. This is not guesswork. It is a formal process where qualified experts examine historical data to produce a legally defensible number.

Whether you are dealing with taxes, a family inheritance, or a legal dispute, getting this number right matters. This article explains what retrospective property valuation is, why you need one, and how the process works.

When do you actually need a historical valuation?

You might wonder, “Why not just use today’s value and adjust backward?” The short answer is that you cannot. Property markets move in response to economic conditions, interest rates, and local trends that existed at a particular point in time.

A retrospective valuation anchors the price to only what the market reflected on that specific date. Here is a breakdown of who uses this service and why.

Top Reasons People Request a Retrospective Property Valuation

Capital Gains Tax (CGT) Calculations: This is one of the most common reasons. If you sell a property you did not live in, you pay tax on the profit. But if you inherited it, or it became a rental years after you bought it, you need the value at that specific starting point to calculate your true gain. Tax authorities typically require a supportable, evidence-based figure for this purpose.

Deceased Estates and Probate Valuation: When someone passes away, their assets generally need to be valued as of the date of death. Many estate and probate processes require you to report asset values as of that specific date, and a formal valuation may be required or strongly recommended depending on your jurisdiction, the complexity of the estate, and the risk of dispute.

Family Law and Divorce Settlements: Splitting assets in a separation is not always about today’s prices. Courts may need to know what a home was worth on the date the couple separated. A retrospective report provides that specific figure to support a fair division.

Resolving Legal Disputes: When partners in a business fall out, or there is a disagreement over a past contract or transaction, courts often require an independent expert to determine what a property asset was worth at the time of the dispute.

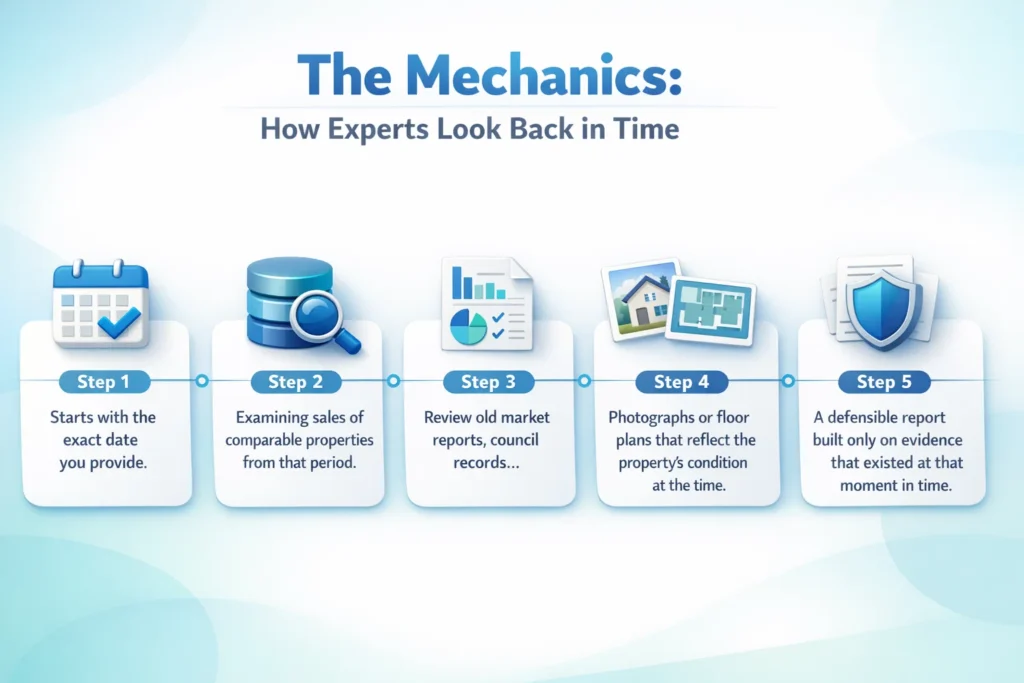

The Mechanics: How Experts Look Back in Time

So how does a valuer actually do retrospective property valuation? The process is detailed and relies on solid historical evidence.

A qualified, independent valuer starts with the exact date you provide. They then work through historical databases, examining sales of comparable properties from that period. They review old market reports, council records, and, where available, photographs or floor plans that reflect the property’s condition at the time.

In some cases, a valuer may inspect the property today to understand its characteristics, but they anchor all conclusions to historical market evidence and what the property’s condition was as of the retrospective date.

The result is a defensible report built only on evidence that existed at that moment in time.

Probate Valuation: A Deeper Look

Because probate valuation is one of the most common requests, it is worth examining probate valuation more closely. Requirements vary by jurisdiction, but in many places you are expected to declare asset values as part of the probate or estate administration process, typically using the open market value as of the date of death.

In some jurisdictions, estate value can be one factor in determining whether simplified procedures are available, alongside other considerations such as asset types, ownership structure, and local rules.

The date-of-death value can also be used to establish the tax starting value (sometimes called cost basis) for beneficiaries when they later sell the property, though the precise rules depend on the tax legislation in your country. Using a qualified, independent valuer ensures this figure holds up to scrutiny from tax authorities and other interested parties.

Retrospective Property Valuation vs. Current Valuation: A Quick Comparison

Still working out the difference? This table breaks it down simply.

| Feature | Retrospective Valuation | Current Valuation |

| Purpose | To determine the value for a past event (tax, death, dispute) | To determine the value for a present decision (selling, refinancing) |

| Valuation Date | A specific date in the past | Today’s date |

| Data Used | Historical market data, past comparable sales | Current market trends, recent comparable sales |

| Common Use | Capital Gains Tax, probate valuation, and family court | Setting a listing price, securing a loan, and insurance |

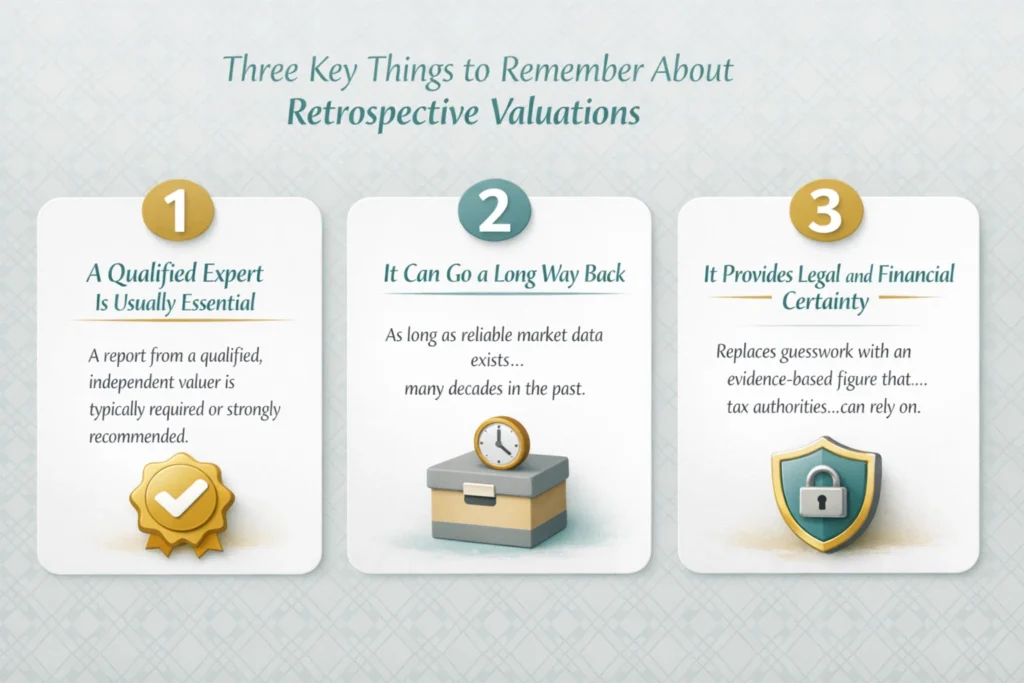

Three Key Things to Remember About Retrospective Valuations

Before you commission a report, keep these points in mind.

1. A Qualified Expert Is Usually Essential

A real estate agent’s informal opinion will generally not satisfy tax authorities or courts. For matters involving tax compliance, estate administration, or legal proceedings, a report from a qualified, independent valuer is typically required or strongly recommended. These professionals have access to historical market data and produce work that follows recognized industry standards, making the result far more defensible if challenged.

2. It Can Go a Long Way Back

Valuers are not limited to just a few years. As long as reliable market data exists for that period, a retrospective valuation can often be produced for properties many decades in the past. In some cases, valuers can even assess properties that have since been demolished, drawing on old records and photographs.

3. It Provides Legal and Financial Certainty

In disputes or tax matters, an unsupported estimate is risky. A formal retrospective report replaces guesswork with an evidence-based figure that all parties, including tax authorities, can rely on. It helps protect you from penalties and supports fair outcomes for beneficiaries or separating parties.

Frequently Asked Questions

How far back can a retrospective property valuation go? There is no fixed cutoff. As long as reliable historical market data exists for the area, a qualified appraiser can typically produce a valuation going back many decades.

The further back the date, the harder it may be to find comparable sales records and property condition documentation, but experienced appraisers are trained to work with older MLS records, county assessor data, and archival sources to build a defensible report.

Does the appraiser need to physically visit the property? Not always, though it depends on the situation. An appraiser may inspect the property today to understand its layout, size, and condition, but they will anchor all conclusions to what the property and market looked like on the retrospective date, using historical records and photographs as supporting evidence.

In some cases, particularly when the property has changed significantly or the retrospective date is very far back, the appraisal may be completed entirely from historical documentation without a current inspection.

Will the IRS or a court accept a retrospective property valuation? Yes, provided it meets the required standards. The IRS expects retrospective appraisals to include well-supported market data, documented comparable sales, and a clear explanation of the methodology used.

Appraisers must follow the Uniform Standards of Professional Appraisal Practice (USPAP) and, for federal tax purposes, meet the IRS definition of a “qualified appraiser.” A report that lacks proper documentation or credentials can be rejected, which may result in penalties or disputes, so working with a licensed, experienced appraiser is essential.

Getting the Right Retrospective Property Valuation for Your Situation

Sorting out historical asset values to resolve present financial matters can feel overwhelming. But an accurate figure is the foundation of every smart decision that follows, whether you are administering a loved one’s estate, addressing a capital gains tax liability, or navigating a legal settlement.

At Bookman Capital, we understand that value requires context, history, and precise data. While we specialize in the valuation of modern SaaS and digital businesses, we respect the rigor required across all asset classes. Accurate, evidence-driven reports are central to everything we do.

Ready to get a clear picture of what your assets are truly worth?

Contact Bookman Capital today for a confidential consultation. We will help you understand your business’s value and guide you toward your next move with confidence.

Sources:

- IRS (Internal Revenue Service)—Topic No. 703: Basis of Assets, and Publication 551 on cost basis rules for inherited property.

- IRS Topic No. 703, Basis of Assets: A concise IRS overview of how basis is calculated for various asset types, including inherited and gifted property

- American Society of Appraisers (ASA)—The leading US credentialing body for professional appraisers, including real property valuation standards.

- The Appraisal Foundation—publisher of the Uniform Standards of Professional Appraisal Practice (USPAP), the nationally recognized standard for appraisals used in US tax and legal proceedings.