Market Approach and Income Approach are the two fundamental methodologies that determine your company’s 409A valuation. Getting a 409A valuation feels tricky, but understanding the methodology behind it doesn’t have to be. When you need to set a stock price for your employees’ options, the IRS requires you to determine fair market value. Two primary methods dominate this calculation: the market approach and the income approach.

These methods draw from different company data and follow distinct logical frameworks. Your startup’s stage and characteristics largely determine which approach appraisers will emphasize in your valuation report.

This guide breaks down both methods, compares them directly, and explains how professional appraisers make their methodological choices.

What is a 409A Valuation Anyway?

A 409A valuation establishes the fair market value of your company’s common stock. This is required by IRC Section 409A when you issue employee stock options. The valuation sets the legal exercise price for those options, ensuring compliance with federal tax law.

You can learn more about the fundamentals in our detailed guide, What is a 409A Valuation?.

The Market Approach: Letting the Market Decide

The market approach values your company by examining comparable market data. It looks at similar businesses that were recently sold or that currently trade on public markets.

At its core, this method operates on a straightforward premise: your business is worth something similar to what the market has recently paid for comparable companies.

Appraisers implementing this approach identify peer companies and calculate standard valuation multiples. Common multiples include Price-to-Revenue or Price-to-EBITDA. They apply these multiples to your company’s financial metrics.

The result is an equity value benchmarked against real market transactions rather than theoretical projections.

Key Characteristics of the Market Approach:

- Foundation: Recent market transactions and current trading prices of comparable companies

- Best For: Companies with substantial revenue and clearly identifiable market comparables

- Data Required: Financial and valuation metrics from similar public companies or M&A transactions

- Output: A value anchored to observable market behavior

Common Market Approach Methods

Professional appraisers typically employ two techniques under the market approach framework. They often use both to triangulate a more reliable valuation.

1. The Comparable Company Analysis (CCA)

This method benchmarks your company against publicly traded peers. The appraiser constructs a peer group that mirrors your industry, growth trajectory, and business model. Then they analyze the trading multiples for this cohort.

Because your private shares lack the marketability of public stock, appraisers apply a discount for lack of marketability (DLOM). This can range from 20% to 40% depending on various factors.

This method proves particularly valuable for later-stage startups with established revenue streams and clear public market analogues.

2. The Precedent Transaction Analysis (PTA)

Rather than examining ongoing trading activity, this method studies completed acquisitions of entire companies within your sector. The appraiser calculates the multiples paid in these M&A transactions. These typically include a control premium reflecting what buyers actually paid to acquire 100% ownership.

When your industry has experienced robust acquisition activity, this method provides valuable real-world validation. This has been especially true in sectors like SaaS, fintech, or healthtech over recent years.

The Income Approach: Valuing Future Potential

The income approach takes a fundamentally different perspective. It values your company based on its projected future cash flows, which are then discounted back to present value.

The primary tool here is the Discounted Cash Flow (DCF) analysis. Financial theorists consider this the most intellectually pure valuation method. It derives value from the company’s own economic characteristics rather than market sentiment.

A DCF model projects your company’s unlevered free cash flow over a five-to-ten-year forecast period. It estimates a terminal value for cash flows beyond that horizon. Then everything gets discounted back to the present using a risk-adjusted discount rate. This is typically the Weighted Average Cost of Capital (WACC).

The sum of these discounted values yields the enterprise value. Equity value is derived after accounting for debt and preferred stock.

Key Characteristics of the Income Approach:

- Foundation: Projected future financial performance adjusted for execution risk

- Best For: Early-stage companies, those with unique business models, or businesses where future potential significantly exceeds current metrics

- Data Required: Detailed financial forecasts, capital structure assumptions, and a carefully calibrated discount rate

- Output: An intrinsic value reflecting the company’s specific projected economics

Building a Discounted Cash Flow Model

The DCF methodology follows a structured analytical process. It requires both financial rigor and reasoned judgment.

- Forecast Period: The appraiser develops detailed financial projections, typically spanning five years. These are based on management’s business plan adjusted for achievability and market conditions.

- Free Cash Flow: For each forecast year, the model calculates unlevered free cash flow. This is the cash available to all capital providers after operating expenses, taxes, and necessary capital investments.

- Terminal Value: The appraiser estimates the company’s value beyond the explicit forecast period. They commonly use the Gordon Growth Model with a perpetual growth rate of 2-4%.

- Discount Rate: The WACC is calculated by weighing the cost of equity (often derived using the Capital Asset Pricing Model) and the cost of debt. This reflects the specific risk profile of the business.

- Present Value: All future cash flows and the terminal value are discounted back to today’s dollars using the WACC.

Market Approach vs. Income Approach: A Direct Comparison

| Feature | Market Approach | Income Approach |

| Primary Data Source | Market prices of comparable companies and transactions | The company’s own projected financial performance |

| Time Perspective | Backward-looking (based on historical transactions) | Forward-looking (based on future forecasts) |

| Best Suited For | Mature companies with revenue and clear market peers | Early-stage or unique companies without reliable comparables |

| Key Inputs | Valuation multiples from public markets and M&A deals | Revenue growth, margin expansion, capital needs, discount rate |

| Major Challenge | Finding truly comparable companies with similar characteristics | Creating reliable long-term forecasts in uncertain environments |

| Subjectivity Level | Lower (market-driven data) | Higher (forecast-dependent) |

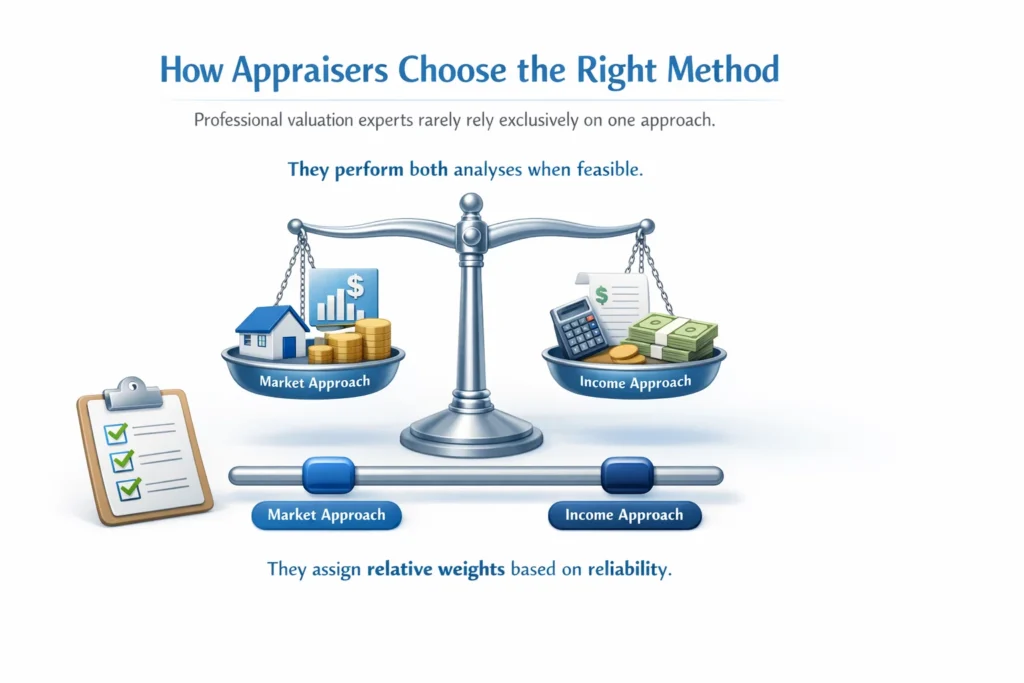

How Appraisers Choose the Right Method

Professional valuation experts rarely rely exclusively on one approach. Instead, they perform both analyses when feasible. Then they assign relative weights based on which method provides more reliable indications of value, given your company’s specific circumstances.

The final 409A report will articulate this weighting decision with supporting rationale.

The weighting decision is industry-specific and highly nuanced. A fintech company with proven revenue might receive 70% weighting on the market approach and 30% on the income approach. A pre-revenue AI startup might see the reverse.

Appraisers consider multiple factors. These include revenue stability, availability of comparables, forecast reliability, and whether your business model has established market validation.

When the Market Approach Receives Greater Weight:

- Your company has established recurring revenue streams with demonstrated customer retention

- Numerous similar public companies or recent M&A transactions provide robust comparable data

- Your business model represents a proven category within your industry

- The competitive landscape and market dynamics are relatively stable and predictable

When the Income Approach Receives Greater Weight:

- Your company is pre-revenue or in very early commercial stages, where current metrics don’t reflect potential

- Your technology, business model, or competitive positioning is genuinely differentiated or novel

- The company’s fundamental value proposition centers on future growth potential rather than current performance

- You operate in an emerging market or technology category where comparable transaction data is sparse or unreliable

Two Critical Listicles for Founders

Five Signs Your 409A Should Lean on the Market Approach

- You can identify at least three to five public competitors with similar financial profiles. They should have comparable growth rates and business models that trade with reasonable liquidity.

- Your industry has experienced frequent merger and acquisition activity over the past 12-24 months. This provides ample transaction data.

- Your financial forecasts are highly uncertain or volatile. This makes income approach projections less reliable than market-based benchmarks.

- Your revenue streams demonstrate predictability and stability. You have high gross retention rates and low customer concentration.

- Sophisticated investors in your cap table frequently reference market comps and trading multiples. They use these when discussing your valuation in financing discussions.

Four Times the Income Approach is Non-Negotiable

- You’re a pre-revenue biotech, therapeutics, or deep technology startup. Current metrics provide virtually no indication of potential value.

- Your company is genuinely pioneering a new category where no meaningful comparables exist. You’re not just incrementally better, but fundamentally different.

- Available market comparables are either far larger (creating size premium issues) or operate in adjacent but materially different business models.

- Your value proposition fundamentally hinges on future technology validation, regulatory approval, or market creation that hasn’t yet occurred.

Frequently Asked Questions

Can a 409A valuation use both methods?

Absolutely, and this is actually the preferred approach among experienced appraisers. By performing separate calculations using both the market approach and income approach, then assigning appropriate weights to each result, the final valuation becomes more defensible and credible.

This blended methodology demonstrates thoroughness. It also reduces the risk that any single method’s limitations could significantly distort the conclusion.

Which method typically produces a higher valuation?

There’s no consistent pattern here. The relationship between methods varies dramatically based on the company stage and market conditions.

The income approach can generate higher valuations for high-growth companies with ambitious but credible forecasts. This is particularly true when comparable companies trade at depressed multiples.

Conversely, the market approach might yield higher values when your sector experiences multiple expansions. It can also produce higher values when your forecasts are conservative relative to market expectations.

The goal isn’t to maximize valuation but to arrive at an accurate, supportable fair market value.

Does the valuation method affect my employees’ stock options?

It affects them indirectly through its impact on the calculated fair market value. The chosen method influences the final FMV determination. This directly sets the exercise price (strike price) for stock options granted.

A higher fair market value means employees will pay more per share when exercising their options. This increases their upfront cost but doesn’t change the ultimate value they can capture if the company appreciates.

The critical objective is reaching an accurate, defensible price rather than manipulating methodology to achieve a desired outcome.

How often should we update our 409A valuation?

To maintain safe harbor protection from IRS challenges, you should obtain a new valuation at least every twelve months. Beyond this annual cadence, you’ll need an updated valuation following any material event.

Material events include new funding rounds, significant changes in financial performance (either positive or negative), major product launches, strategic pivots, or changes in market conditions that materially affect your company’s risk profile.

An outdated report loses its protective value. This potentially exposes both the company and option recipients to the Section 409A penalties described earlier.

Get Your Confident 409A Valuation Started

Understanding the methodological frameworks behind 409A valuations represents an important first step in equity compensation planning. The next step involves executing a defensible, audit-ready valuation with a partner who understands both startup economics and valuation standards.

Bookman Capital provides comprehensive, technically rigorous 409A valuations with clear documentation. We satisfy auditors and regulators alike. We explain the process in plain language, walk you through our methodology selection, and deliver analysis that gives you and your team confidence in your option pricing.

Stop worrying about IRS compliance, audit challenges, and whether your option exercise prices can withstand scrutiny. Let’s build a solid foundation for your equity compensation program.

Contact Bookman Capital today to start your valuation.

Sources: